A Yale University study finds that the US jobs market has not yet experienced significant disruption from AI advancements like ChatGPT, with historical trends suggesting that technological impacts on employment typically unfold over decades rather than months.

Goldman Sachs has issued a concerning warning about the jobs market, indicating potential economic challenges ahead based on recent employment data and analysis.

Retail sales in March surged 0.7%, exceeding expectations, as Americans continue to spend despite inflation and economic challenges. Excluding gas prices, retail sales rose 0.6%. The strong sales were attributed to a robust job market and rising wages, with general merchandise and online sales seeing increases while department stores, furniture, and electronics stores experienced declines. Despite inflationary pressures, the Federal Reserve is unlikely to cut interest rates soon, as core prices rose 0.4% from February to March and 3.8% year-over-year. Economists anticipate consumer spending to moderate due to less optimism about economic prospects and high living costs.

Canaccord Genuity's chief market strategist, Tony Dwyer, believes that the Federal Reserve needs to be more aggressive with rate cuts due to a weakening jobs market and easing inflation. Dwyer points to falling employment survey participation rates skewing jobs report data and expects the Fed to act in response. He anticipates rate cuts to benefit financials, consumer discretionary, industrials, and health care stocks, leading to a more even market performance by the end of the year.

The U.S. jobs market exceeded expectations in November, with nonfarm payrolls rising by 199,000 and the unemployment rate dropping to 3.7%. Average hourly earnings also increased more than anticipated. Inflation expectations among consumers have plunged, with the University of Michigan consumer sentiment survey showing a significant drop in one-year inflation rate expectations. This, along with a strong jobs report, has boosted market optimism for a "soft landing" scenario. Additionally, China's consumer price index fell sharply in November, while producer prices also dropped. Investors will closely watch upcoming inflation reports and the Federal Reserve's final meeting of the year for further insights into the economic outlook.

The November jobs report is expected to show an acceleration in job growth due to the return of striking UAW and SAG-AFTRA workers, with an estimated boost of 45,000 jobs. Adjusted for these strikes, job growth is projected to be around 160,000, down from 183,000 in October. The impact of the auto strike on employment in the manufacturing sector was reflected in the October jobs report, with a decline of 35,000 jobs. Additionally, labor disputes in the motion picture and sound recording industries have led to a decline of 44,000 jobs since May. Despite the strike-related noise, the jobs report is expected to reflect softening labor market conditions, potentially allowing the Federal Reserve to hold off on further rate increases.

The US job market is showing signs of softening as new data reveals slower payroll growth, particularly in the leisure and hospitality sector. ADP reported that the US added 103,000 private payroll jobs in November, below economists' expectations. This slowdown in job creation suggests that the economy as a whole will experience more moderate hiring and wage growth in 2024. Additionally, the latest Job Openings and Labor Turnover Survey (JOLTS) report indicates a decrease in the ratio of job openings to unemployed workers, while wage growth for workers changing jobs has slowed down. Despite these signs, the stock market opened higher on Wednesday.

US stocks rose as investors reacted to data indicating a slowdown in the labor market, with the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite all posting gains. The ADP gauge on private payrolls missed expectations, revealing that 103,000 jobs were added in November. This follows Tuesday's soft reading on job openings, which increased optimism for a Federal Reserve interest rate cut. Bitcoin briefly surged past $44,000 before retracing its gains, as retail investors embraced hopes for rate cuts and upcoming spot bitcoin ETFs.

The jobs market remains tight, with limited opportunities for job seekers, as corporate, financial, and political developments continue to impact employment prospects worldwide.

Consumer spending in the U.S. rose sharply by 0.7% in September, exceeding expectations and indicating the strength of the economy. Outlays grew by 4% in the third quarter, the largest increase since 2019 excluding pandemic years. However, after adjusting for inflation, incomes fell for the third consecutive month. Americans spent more on services, including travel and healthcare, but rising costs of necessities played a role. Consumer spending adjusted for inflation increased by a more modest 0.4%. The savings rate declined to 3.4% from 4%, leaving households with less financial cushion. The PCE price index, a key inflation measure, rose higher than expected by 0.4% in September. Despite expectations of a slowdown in spending, a strong jobs market is likely to support continued economic expansion.

Mortgage rates are currently high, making it challenging for potential homebuyers. However, there is a possibility of some relief in 2024. Three ways mortgage rates could fall include potential rate cuts by the Federal Reserve, a decrease in inflation, and a cooling down of the job market. While rates are unlikely to reach the levels of 2020 and 2021, these factors could lead to a slight dip in mortgage rates next year.

The US jobs market continues to defy expectations as employers added 336,000 jobs in September, with unemployment remaining at 3.8 percent. Additionally, there were upward revisions to job creation in July and August. However, the economy shows signs of divergence, with some sectors and states experiencing growth while others struggle. Persistent inflation, high interest rates, and strikes contribute to the two-faced nature of the economy. Economic inequality is also a concern, with the wealthiest becoming richer while poverty rates increase and real wages fall for others. Overall, the jobs report is positive, but questions remain about the overall health of the economy.

The US jobs market remains steady, but there are mixed signals from different sources of data. Private payroll processor ADP and the Bureau of Labor Statistics (BLS) often produce different estimates of monthly job hires, making it difficult to determine the true state of the labor market. The Federal Reserve closely monitors the labor market to gauge signs of a slowdown and determine whether more rate hikes are needed to cool the market and control inflation. While ADP and BLS data have their limitations and variations, they provide valuable insights when used together, and blending their sources of data could potentially offer a more accurate view of the labor market.

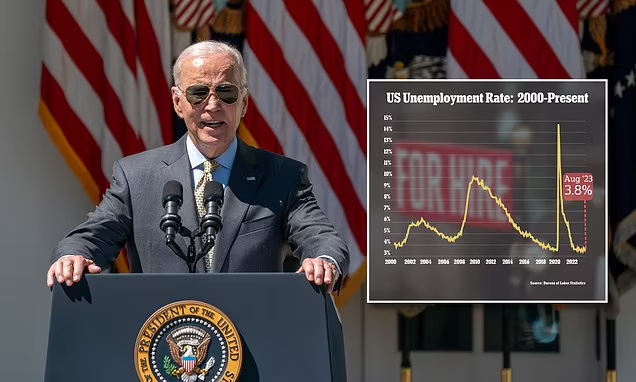

President Joe Biden mistakenly claimed that unemployment had been below 14% for the past 19 months, when he actually meant it had been below 4%. The jobless rate rose to 3.8% in August, the highest since February 2022, according to the Labor Department. Biden touted his administration's job growth and recovery efforts, but critics pointed out that former President Donald Trump's term began with job growth and ended with a pandemic-induced economic shutdown. The rising unemployment rate suggests a cooling labor market, which could help tame inflation, according to the Federal Reserve.