The stock market experienced significant growth in 2025, driven by resilient earnings, interest rate cuts, and enthusiasm for AI, with experts optimistic about continued gains in 2026, despite some risks and uncertainties.

Fed Chair Powell indicated a potential rate cut due to rising downside risks to employment and economic weakening, while emphasizing that any decision will depend on data and risk assessment, amidst political pressures and trade tensions.

Federal Reserve Chair Jay Powell indicated that the shifting economic risks are increasing the case for a rate cut to support the economy, amid uncertainties that could influence future monetary policy decisions.

Veteran hedge fund manager Doug Kass warns that the recent stock market rally, driven by speculation and algorithmic trading, masks underlying risks such as economic slowdown, rising tariffs, and high valuations, suggesting investors should exercise caution and consider holding cash amid potential downturns.

Economists warn that the significant increase in the US federal deficit due to Trump's tax and spending bill could lead to dangerous economic consequences, including higher interest rates, reduced government flexibility in crises, and potential a doom loop of rising debt and interest costs, threatening long-term economic stability.

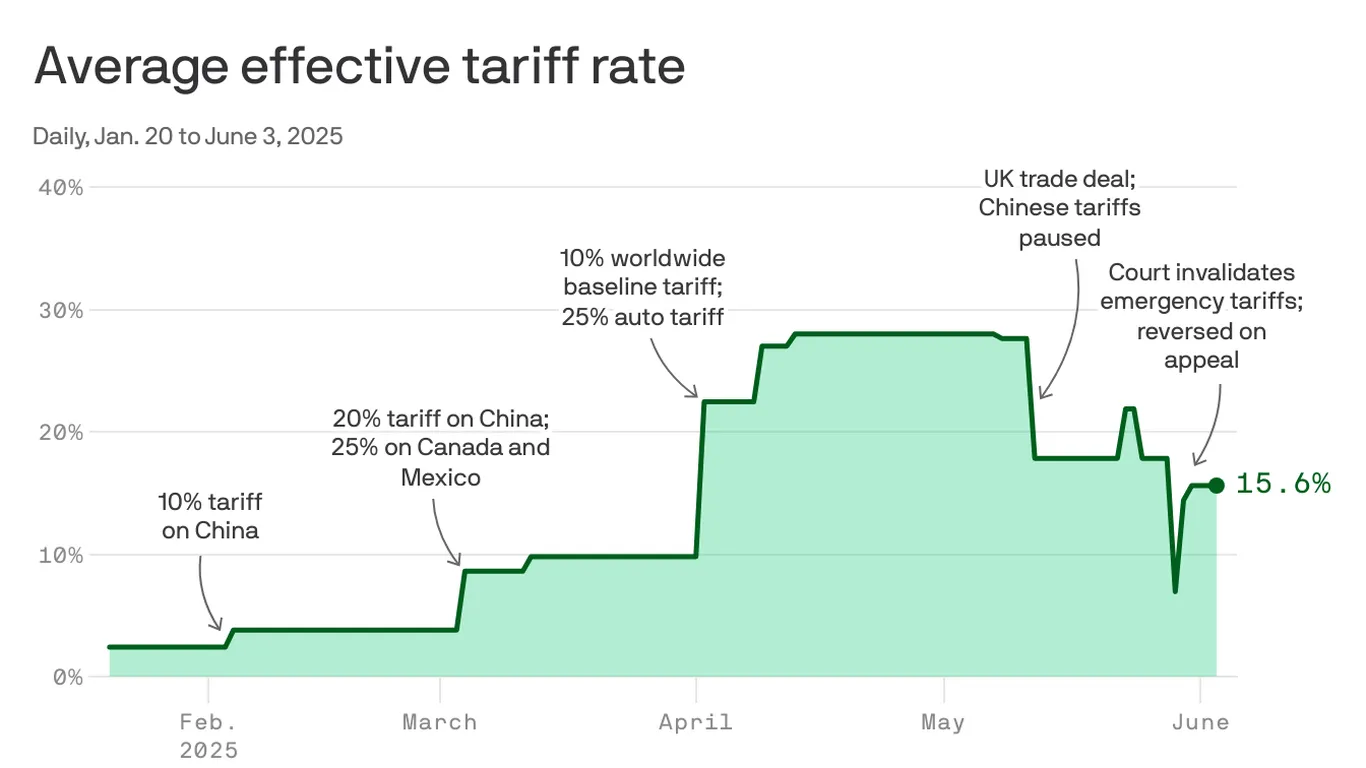

Since February, President Trump has rapidly and unpredictably changed U.S. trade policy, leading to higher and more volatile tariffs that create significant economic risks and supply chain uncertainties for businesses, with tariffs fluctuating dramatically within short periods and complicating long-term planning.

The Financial Times argues that it's acceptable to be complacent about economic risks in the Red Sea, but readers must subscribe to access the full article and understand the reasoning behind this perspective.

As global leaders convene in Davos, the global economy in 2024 is expected to experience a soft landing with anticipated interest-rate cuts to bolster growth and markets worldwide. However, potential threats loom, including the impact of the Houthis, hyperinflation, and other risks stemming from years of conflict, pandemic, and financial instability.

Project Syndicate commentators highlight key issues for 2024, including threats to democracy, the impact of major wars, and economic challenges. They emphasize the importance of democratic elections in addressing these issues and maintaining democracy's future. Africa faces particular challenges with coups, conflicts, and climate change, with countries like Nigeria and regions like the Sahel and Horn of Africa under significant stress. Despite these challenges, there is hope that innovative solutions and a resilient political center can counteract destructive political movements.

The gold market outlook for 2024 is influenced by the Federal Reserve's plan to cut interest rates, which will put upward pressure on gold prices. Economic and geopolitical risks, such as global economic slowdown and conflicts in the Middle East and Ukraine, also make gold an attractive asset for wealth protection. From a technical analysis perspective, the market is bullish, with attention on the $2000 level and the 50-Week EMA. The $1800 level is seen as a strong support level. Overall, while the value of gold may be affected by central banks cutting rates, it remains a reasonable asset for portfolio diversification.

China has instructed state-owned banks to extend the terms, adjust repayment plans, and reduce interest rates on existing local government debt in an effort to mitigate debt risks and support the faltering economy. Local government debt in China has reached 92 trillion yuan ($12.58 trillion), representing 76% of the country's economic output. The debt restructuring measures aim to prevent defaults and ensure banks do not incur heavy losses. The People's Bank of China (PBOC) will also establish an emergency liquidity tool to provide short-term loans to local government financing vehicles (LGFVs). The move comes as China faces a deepening property crisis and mounting economic risks.

JPMorgan Chase CEO Jamie Dimon believes that U.S. interest rates "may go up more" but hopes for a soft landing. He acknowledges the risks of an economic hard landing, including factors such as Ukraine, oil, gas, war, and Europe. Dimon cautions that the current economic optimism may be a temporary "sugar high" and emphasizes the need to address serious issues and unsustainable deficits. He advises clients to prepare for potential stress in the system and warns that a 7% interest rate scenario could be challenging. The Federal Reserve has left the benchmark interest rate unchanged, but the possibility of further rate hikes remains.

China's property market is facing significant challenges, with rising debt levels and a potential bubble. This poses risks to the country's banks, which are caught in an "impossible trinity" of balancing economic growth, financial stability, and controlling debt. The situation highlights the need for China to address its property mess and implement measures to mitigate the risks to its banking sector.

Chinese leaders are planning a range of measures to address the risks posed by local government debt, including special bond issuance, debt swaps, loan rollovers, and potentially dipping into the central budget. Local governments in China have accumulated significant debt due to over-investment in infrastructure, declining returns from land sales, and the impact of the COVID-19 pandemic. The extent of Beijing's involvement and the conditions attached to it are still uncertain, but economists believe that decisive and long-lasting measures are necessary to address the municipal debt crisis. The central government may instruct state-owned banks to roll over maturing debt, while local governments could issue bonds to swap for off-balance sheet debt. Beijing may also issue low-cost bonds to replace local debt. However, profound changes to the Chinese economy will be needed to prevent the problem from recurring in the future.

JPMorgan Asset Management's CIO, Bob Michele, warns investors to be cautious of the ongoing stock market rally as it is reminiscent of the months leading up to the 2008 financial crisis. He cites the Federal Reserve's aggressive interest-rate increases, credit squeeze caused by banking-sector stress, risks tied to commercial real estate, and the inverted bond-yield curve as indicators of looming economic risks. Michele believes it would be a "miracle" if the US economy avoided a recession once the Fed's rate hike campaign ends.