China's economy appears resilient with strong exports and technological advances, but many ordinary Chinese face economic hardships due to weak property prices, job insecurity, and reduced household incomes, leading to a disconnect between official growth figures and public sentiment.

In 2024, inflation offset income gains for most Americans, keeping household incomes steady, though the wealthiest 10% saw increases and women and Black people experienced losses, according to the U.S. Census Bureau.

The August 2025 survey from the Federal Reserve Bank of New York shows a slight increase in short-term inflation expectations, worsening job and unemployment outlooks, and a decline in job finding prospects, while household income growth remains stable and credit perceptions fluctuate.

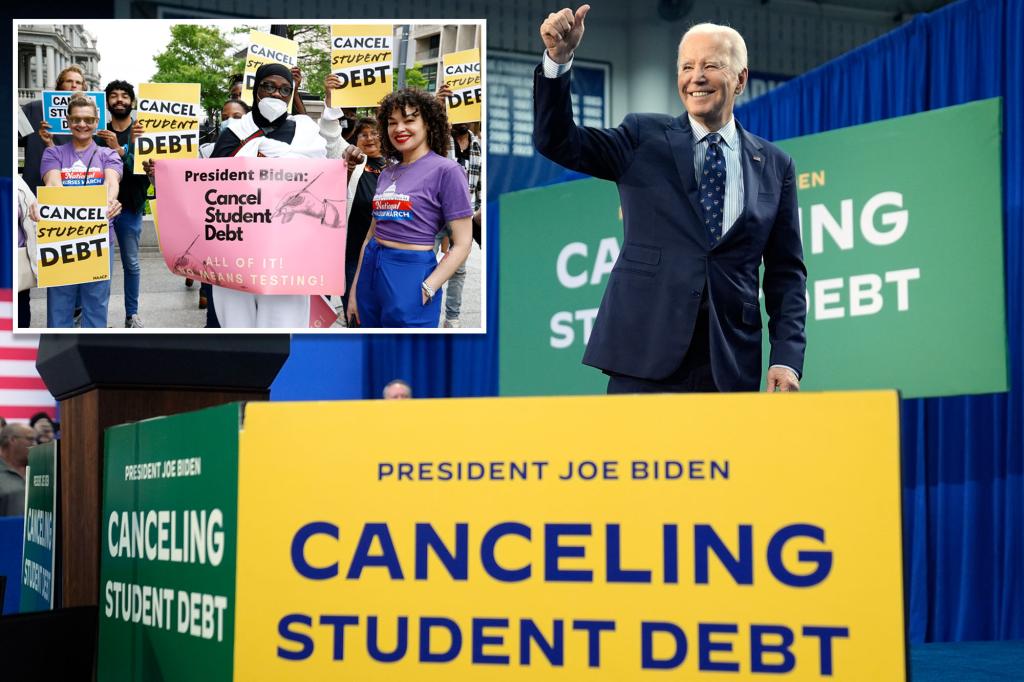

President Biden's student loan cancellation plans are estimated to cost taxpayers $559 billion, with households earning over $300,000 benefiting the most, according to a study by the University of Pennsylvania. The new plan will relieve longer-term student debt for about 750,000 households with an average income of over $312,000, drawing criticism from House Budget Committee Chairman Jodey Arrington. The Penn Wharton Budget Model does not account for the administration's additional $7.4 billion student debt cancellation announcement, and at least 10% of borrowers have been approved for some debt relief under the Biden administration's various student loan cancellation programs.

According to Realtor.com, homebuyers in nearly half of the country need to earn at least six figures to purchase a home, with the typical household needing to earn $99,000 nationally to afford a median-priced home of $415,500 in February. The analysis also considers property taxes and insurance costs, assuming a 10% down payment. The surge in home prices since the COVID-19 pandemic and the increase in mortgage rates have made it financially challenging for many households to afford a home. In 23 states, buyers needed to earn at least $100,000 to avoid spending more than 30% of their gross income on housing, while the typical household income in America was only about $75,000 in 2022.

Housing affordability in the U.S. has significantly worsened, with the typical household needing to earn $113,520 annually to afford the median home, 35% more than the average household income. Affordability has been strained due to high home prices, a shortage of starter homes, and recent layoffs in the technology industry. While borrowing costs are expected to decrease and inventory to increase, experts caution that the housing market's outlook remains uncertain.

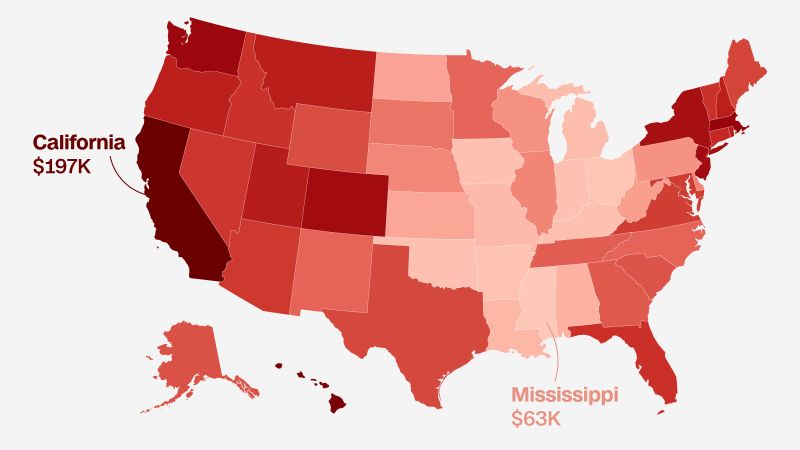

The median household income needed to afford the median-priced home varies widely across US states, with Hawaii requiring the highest income at $153,520 and West Virginia the lowest at $38,320. Meanwhile, 'Million Dollar Listing LA' star discusses how clients are insuring homes amid rising rates, and the price of chocolate is soaring due to supply chain issues.

A new analysis from Bankrate.com reveals that in 22 states and Washington, DC, a six-figure household income is now required to comfortably afford a typical median-priced home, a significant increase from just six states and the District of Columbia in January 2020. Factors contributing to this include rapid home price appreciation outpacing wage growth, limited housing supply, and the "lock-in effect" of higher mortgage rates and home prices. The West Coast and Northeast require the highest household incomes, while the South and Midwest require the lowest. Affordability changes over time are evident in the significant increase in income needed to buy the average home today compared to 2020, with the Sun Belt becoming less affordable due to an influx of new homebuyers.

A new report from Bankrate reveals that car insurance premiums in the US have surged by 26% in 2024, reaching an average of $2,543 annually. This increase means that Americans now spend around 3.41% of their income on car insurance on average. Factors such as population density, driving habits, extreme weather, driving history, vehicle type, and credit history all contribute to the rising costs. Detroit has the highest net average cost of car insurance, while drivers in Seattle spend the lowest percentage of income on car insurance.

The definition of "middle class" varies depending on location and household size. According to Pew Research Center, nationwide, middle income ranges from $52,000 to $156,000 for a family of three. In Oklahoma City, a household would be considered middle class if it earns between $39,984 and $119,358. For an individual in the Oklahoma City metro, making between $25,500 and $76,000 would be considered middle class. However, inflation has increased the cost of living, so these numbers may not go as far as they used to.

The percentage of adults in middle-class households in the US has dropped from 61% in 1971 to 50% in 2021, according to Pew Research Center. In Florida, the minimum annual income necessary for a family of four to be considered middle class in 2023 is $67,835. However, different cities in Florida have different income thresholds for middle-class status, ranging from $39,276 to $117,242 in Jacksonville, $42,974 to $128,282 in St. Petersburg, $32,689 to $97,578 in Miami, and $36,292 to $108,334 in Orlando. The average median household income in Florida is $61,777. The middle class is shrinking, with upper-income households surging forward and lower-income households increasing in number.

The household income in Minnesota continues to decline, leading to an increase in the number of families facing economic hardship and in need of assistance.

New data from SmartAsset shows that there is a nearly $100,000 disparity between household incomes required to be considered middle class in cities across the United States. The data was compiled using the US Census Bureau's American Community Survey and compared the top and bottom thresholds of the middle class across 100 cities, along with the across all fifty states. The west coast dominated the list of wealthiest cities for the middle class, with California cities taking four of the top 10 spots, Arizona cities taking three, and Washington claiming one. Americans facing rising inflation have become nostalgic for prices from just two years ago.

California's three largest power companies have submitted a joint proposal to the state's Public Utilities Commission to simplify electricity bills to include a fixed-rate billing system based on household income. The aim is to lower power bills, particularly for lower-income customers, while increasing transparency. Customers would see two main charges on their bills: a new fixed rate and power use rates. The fixed rate will cover the costs of safely building, maintaining and operating the electric grid, of providing customer support, and the cost of state initiatives to help income-qualified customers and energy-efficiency programs. Income verification would be handled by a third party, possibly a state agency.