The share of risky subprime borrowers at least 60 days behind on auto loans has reached a record high of 6.65% in October, driven by inflation, rising interest rates, and economic pressures, signaling economic weakness and increasing financial strain on consumers.

Auto loan debt in the US has reached $1.66 trillion, with rising delinquencies and repossessions, especially among younger and higher-credit-score borrowers, raising concerns about a potential economic crisis similar to 2008, and prompting calls for congressional action to protect consumers.

In Q2 2025, total household debt increased modestly to $18.4 trillion, with a decline in debt-to-income ratio indicating improved consumer financial health, despite a significant spike in delinquent federal student loans as they re-enter credit reports after forbearance. Foreclosures remain low, and third-party collections are at record lows, but the rise in student loan delinquencies and potential future collection actions pose risks to the credit landscape.

Consumers skipping auto payments, especially among subprime borrowers, signals rising financial stress and potential market dislocation, despite optimistic headlines. This behavior indicates deeper economic issues, with auto loan delinquencies reaching 15-year highs and market mispricing the risk, presenting opportunities for early investors to position ahead of a broader downturn.

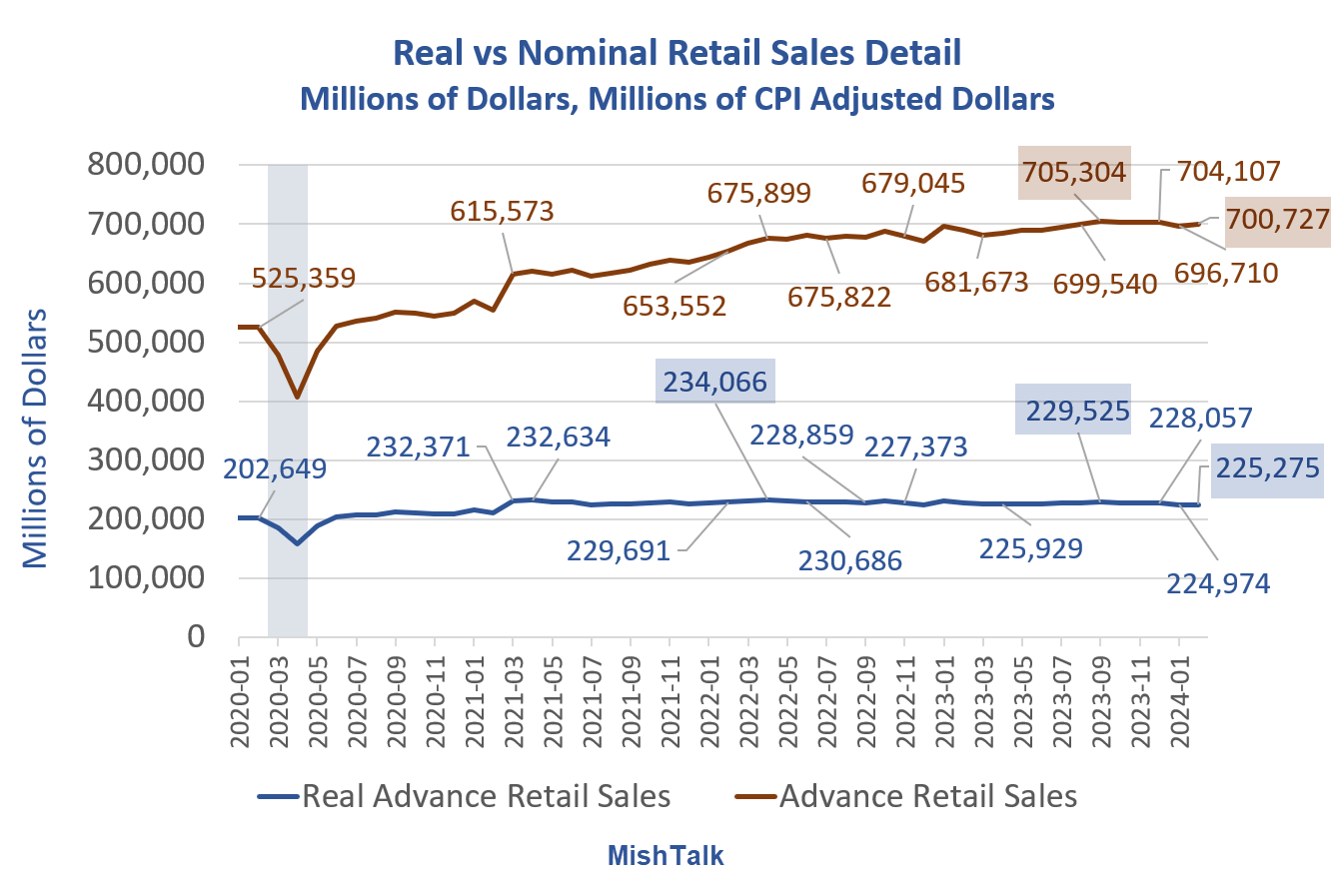

US consumer spending has shown signs of decline since October 2023, with real retail sales weakening despite nominal sales appearing strong. Economic stress is evident, particularly among younger age groups, as credit card and auto loan delinquencies soar to record highs. Homeownership rates also reflect struggles among Millennials and Zoomers. The popularity of "Buy Now, Pay Later" plans indicates consumer credit stress, while job market data reveals a weakening labor market. Additionally, inflation remains high, leading to concerns about stagflation as economic cracks in spending, employment, and delinquencies emerge.

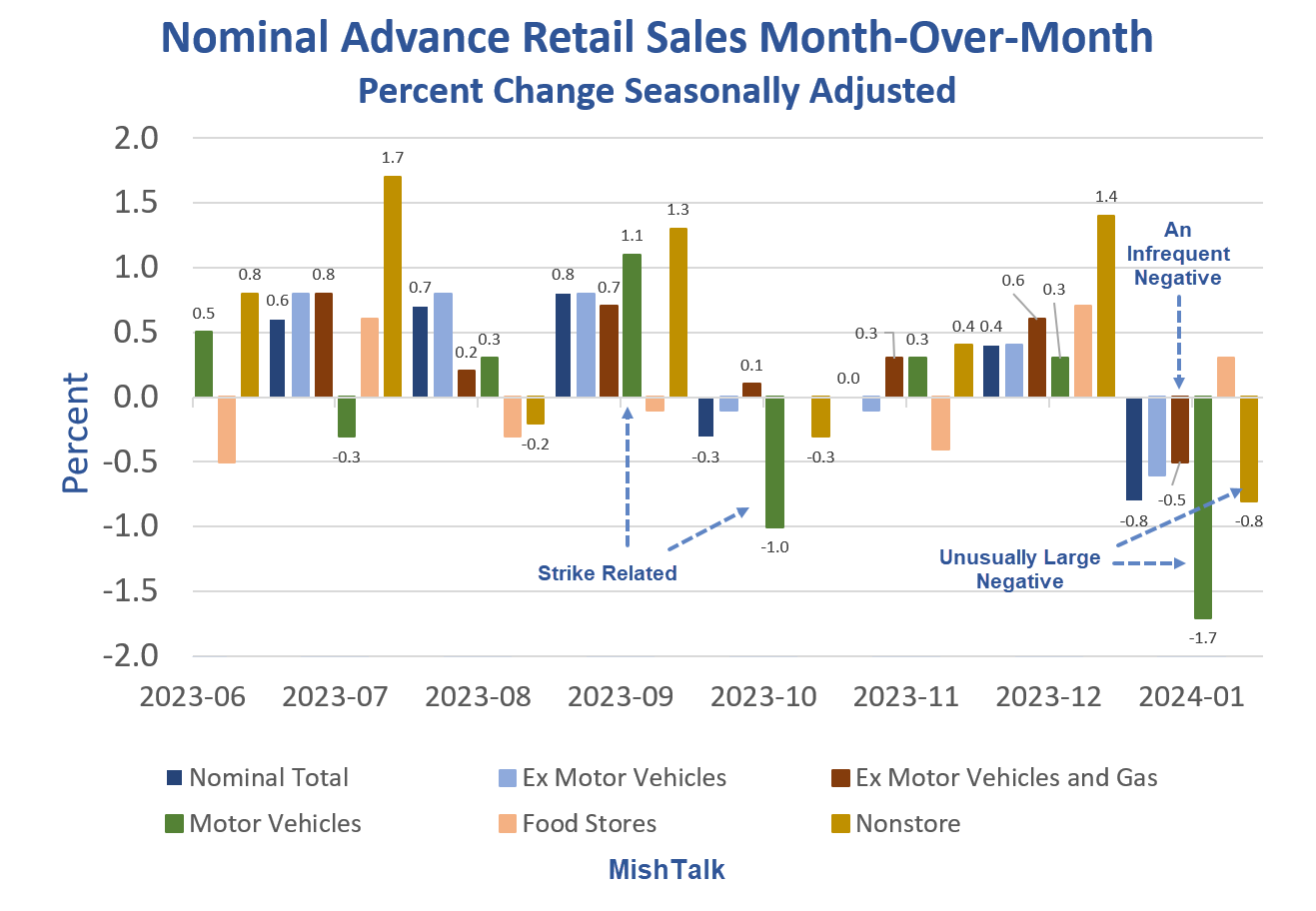

Retail sales unexpectedly dropped by 0.8 percent in January, with negative revisions also impacting December's figures. Despite claims of strong consumer demand, the economy is facing inflationary pressures, as evidenced by declining car and gasoline sales. When factoring in the Consumer Price Index (CPI), the real decline in sales is even steeper. Additionally, credit card and auto delinquencies are on the rise, indicating potential stress on consumer credit.

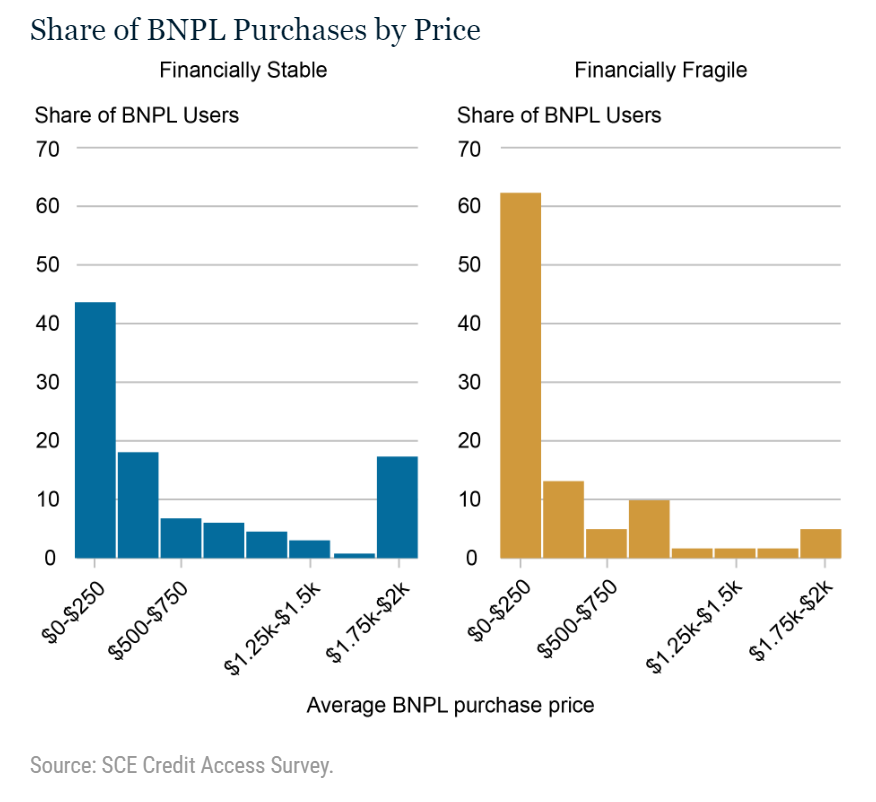

Buy Now Pay Later (BNPL) plans are gaining popularity, particularly among financially fragile individuals, who are more likely to use BNPL at higher frequencies and for medium-size, out-of-budget purchases. The financially stable tend to use BNPL for a few high-priced items to avoid paying interest. However, missing payments can lead to accruing interest, contributing to financial stress and delinquencies, especially among renters facing increasing costs. The study suggests that there is still potential for increased adoption of BNPL, but it also highlights the potential risks and financial implications for users.

Americans' credit card debt has reached a record high of $1.13 trillion, with a $50 billion increase in the fourth quarter of 2023 alone. Total household debt rose to $17.5 trillion, and delinquencies on credit card payments are on the rise across all age groups, particularly among those aged 30-39. Additionally, auto loan balances have also increased, attributed in part to higher car prices following the pandemic.

Americans' total credit card debt hit a record high of $1.13 trillion at the end of 2023, with card balances increasing by 4.6% in the fourth quarter. Credit card delinquencies also rose, contributing to the overall household debt reaching $17.5 trillion. Factors such as higher living costs and more cardholders carrying over debt from month to month have led to increased financial stress, particularly among younger and lower-income households.

The Federal Reserve Bank of New York's Quarterly Report on Household Debt and Credit reveals a $212 billion increase in total household debt in the fourth quarter of 2023, with rising delinquencies in credit card and auto loan transitions, particularly among younger and lower-income households. Mortgage balances, home equity lines of credit, credit card balances, and auto loan balances all saw increases, while delinquency transition rates for credit cards and auto loans rose. The report provides insight into U.S. consumer credit conditions and aims to help various entities better understand and respond to trends in borrowing and indebtedness at the household level.

A report from the New York Fed reveals that low-income borrowers are struggling to make payments on car loans and credit cards, with delinquencies surpassing prepandemic levels. Many missed out on the opportunity to refinance their mortgages during the pandemic, leading to higher monthly payments as current mortgage rates average 6.6%. Low-income areas also have lower levels of homeownership and higher rent burden, with 57% of households spending more than 30% of their income on rent.

Younger consumers are increasingly turning to "buy now, pay later" options as credit card debt and delinquencies rise, with experts warning of a potential credit card crisis. A Bank of America survey revealed that nearly three in four Gen-Zers have reduced their spending due to higher inflation. VantageScore CEO Silvio Tavares noted that banks and credit card lenders are already pulling back, reducing the number of new credit accounts, while buy now, pay later providers continue to see growth. Tavares cautioned that if credit deterioration occurs in the next few months, it could be concerning for consumers who may face difficulty making payments.

The average credit card balance in the US has reached a 10-year high, surpassing $6,000, as inflation and rising costs put pressure on households. Delinquency rates have also increased, indicating that more cardholders are struggling to make payments. The cost of servicing credit card debt has risen significantly, with average annual percentage rates now exceeding 20%. This means that making minimum payments on the average balance would take over 17 years to pay off, incurring over $9,000 in interest. Experts recommend strategies such as balance transfers, refinancing into lower-interest personal loans, or negotiating lower interest rates with card issuers to tackle costly credit card debt.

A record number of Americans are falling behind on their car payments, with the percentage of auto borrowers at least 60 days late on their bills reaching the highest level in nearly three decades. High auto prices, inflation, and rising interest rates have strained household budgets, leading to increased loan delinquencies. While defaults have not yet seen a significant increase, repossessions are expected to climb in the coming months. The average cost of a new car is around $48,000, and the average new auto loan rate has jumped to 7.4% in September. Rising interest rates and high car prices have pushed monthly payments above $1,000 for many Americans, raising concerns for the auto industry.

The rate of subprime borrowers behind on auto loan payments by more than 60 days reached a record high of 6.11% in September, according to Fitch Ratings. This indicates ongoing economic struggles for lower-earning workers amid high inflation, a challenging job market, and the resumption of federal student loan payments. Delinquency rates are expected to continue rising, peaking at around 10% before declining. The high interest rates and increasing reliance on borrowing are contributing factors. Vehicle repossession rates are also on the rise, leaving many without transportation.