President Trump has proposed a one-year cap of 10% on credit card interest rates, aiming to reduce consumer costs, but financial institutions criticize the move, arguing it could limit access to credit.

US consumer credit scores have declined at the fastest rate since the 2008 financial crisis, with Gen Z borrowers experiencing the largest drops due to higher utilization and delinquency rates, especially related to student loans, while the median FICO score continues to rise.

Consumers skipping auto payments, especially among subprime borrowers, signals rising financial stress and potential market dislocation, despite optimistic headlines. This behavior indicates deeper economic issues, with auto loan delinquencies reaching 15-year highs and market mispricing the risk, presenting opportunities for early investors to position ahead of a broader downturn.

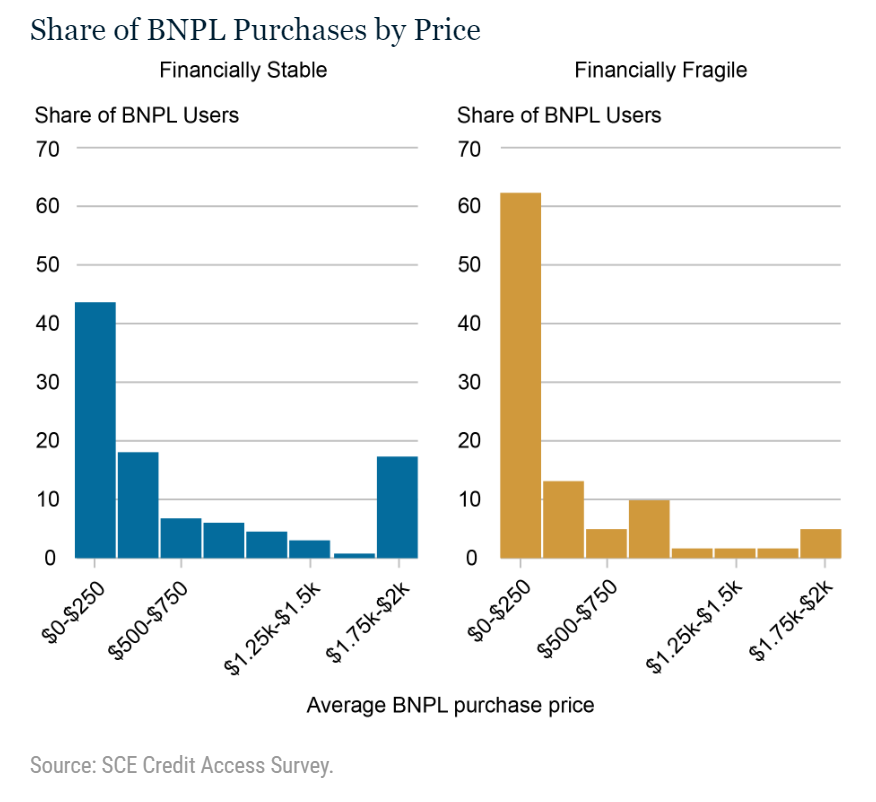

Buy Now Pay Later (BNPL) plans are gaining popularity, particularly among financially fragile individuals, who are more likely to use BNPL at higher frequencies and for medium-size, out-of-budget purchases. The financially stable tend to use BNPL for a few high-priced items to avoid paying interest. However, missing payments can lead to accruing interest, contributing to financial stress and delinquencies, especially among renters facing increasing costs. The study suggests that there is still potential for increased adoption of BNPL, but it also highlights the potential risks and financial implications for users.

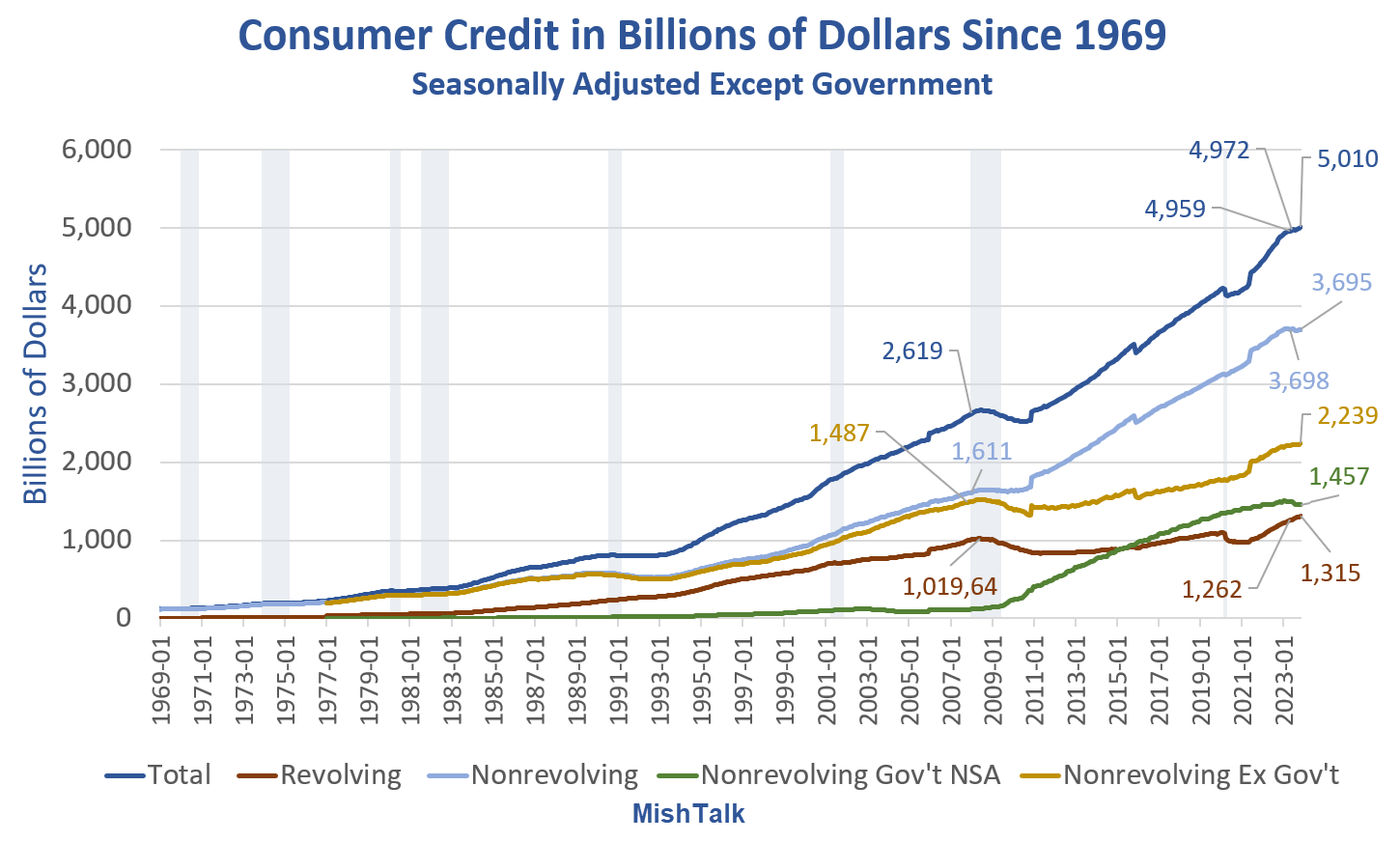

Consumer credit has reached a record $5 trillion, with revolving credit and credit card interest rates also hitting new highs in November. Adjusted for inflation, revolving credit is approaching levels seen during the Great Recession. Credit card rates, which averaged between 12-14 percent for most of 2000-2020, have now reached an average of 21.47 percent. Additionally, a spending deal has been reached, but the Republican Freedom Caucus has condemned it for not addressing border funding, potentially leading to further negotiations.

Apple is set to end its credit card partnership with Goldman Sachs within the next 12-15 months, marking a major setback for the bank. Goldman struggled to scale the required customer service and back-end resources for the program and considered handing it off to other suitors. This move comes after Goldman lost $3 billion on consumer banking since 2020. For Apple, the end of the partnership could hinder its efforts to increase service revenue, which has become crucial as product sales decline. Apple is expected to pursue a credit deal with a new banking partner, although the specific partner remains unknown.

Apple has launched a "buy now, pay later" service in the US, allowing customers to finance purchases made through Apple Pay in instalments over time. The service, called Apple Pay Later, will offer two payment options: "Apple Pay in 4" and "Apple Pay Monthly Installments". The former will allow customers to pay for purchases in four interest-free payments, while the latter will allow customers to finance purchases over several months with interest.