Federal Reserve Faces Uncertain Waters Amid Political and Internal Challenges

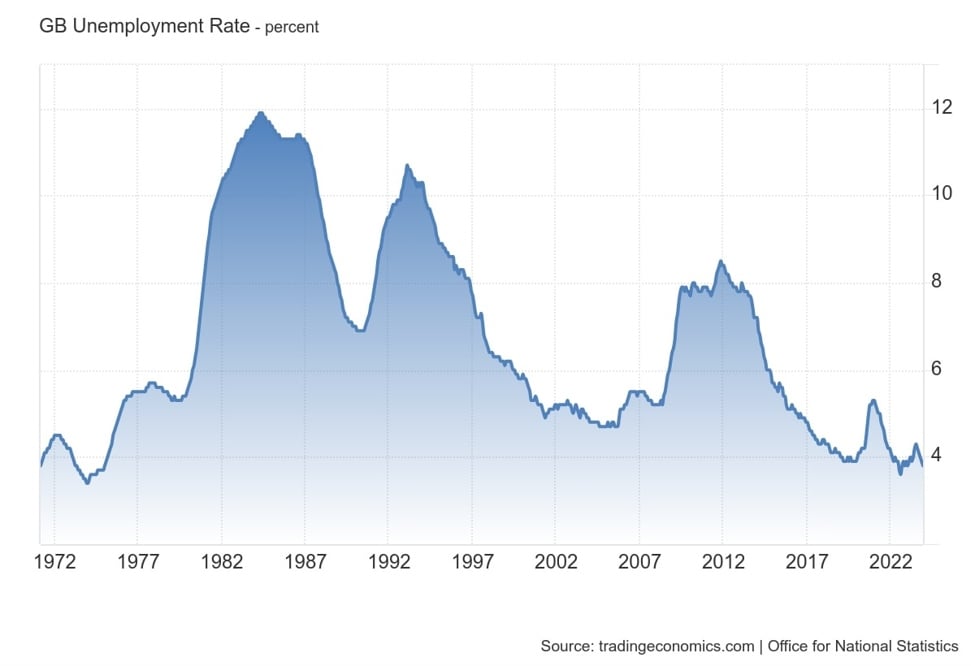

The US Federal Reserve begins its two-day policy meeting amid expectations of a 25 basis-point interest rate cut, with increased political pressure from the White House and recent appointments influencing its independence. Markets are largely in a wait-and-see mode, while UK and US economic data, including labor and retail figures, are also in focus. The Fed's decision and political developments are shaping investor sentiment and market movements.