The U.S. economy is showing strong signs of recovery under President Trump, with consistent inflation control, rising industrial output, record customs revenues, robust retail sales, and declining unemployment claims, indicating a positive economic trajectory.

Asian markets saw mixed performances with South Korean stocks leading declines due to a drop in industrial production for the second consecutive month. The Kospi and Kosdaq indices fell, while China's CSI 300 rose by 2% amid expectations of stabilizing home prices. Japan's inflation data showed an increase, influencing the yen's appreciation. Meanwhile, India's economic growth is projected to slow, and Australia's competition watchdog approved an interim partnership between Virgin and Qatar Airways. Additionally, India's competition authority is investigating Google's gaming app policies.

Despite a property slump leading to the slowest quarterly growth in five quarters, China's technology-driven sectors like EVs, solar, and tech are showing strength, aligning with Xi Jinping's goal for high-quality growth.

China's second-quarter GDP growth of 4.7% fell short of the expected 5.1%, with June retail sales also missing forecasts. However, industrial production exceeded expectations, growing by 5.3%. Urban fixed asset investment met expectations, but infrastructure and manufacturing investment growth slowed, and real estate investment continued to decline. The urban unemployment rate remained steady at 5%. Despite higher-than-expected export growth, weak domestic demand and credit data indicate ongoing economic challenges.

China's economic data for the first two months of the year surpassed expectations, with retail sales rising 5.5%, industrial production increasing 7%, and fixed asset investment rising by 4.2%. However, real estate investment fell by 9%, and retail sales did not rebound as strongly as expected. The country's focus on developing manufacturing and technological capabilities was emphasized, while new support for the real estate sector was not revealed. Additionally, exports for January and February exceeded expectations, rising by 7.1% in U.S. dollar terms.

Germany's economy continues to struggle as recent data shows declines in industrial production, exports, and factory orders. While there are some glimmers of hope, such as a slight uptick in the Purchasing Managers' Index, experts remain cautious about the prospects for economic recovery. Factors such as global rate hikes, high energy prices, and political challenges within the coalition government are contributing to the uncertainty, with some forecasting a modest contraction in the first quarter of 2024 and a flat full-year growth.

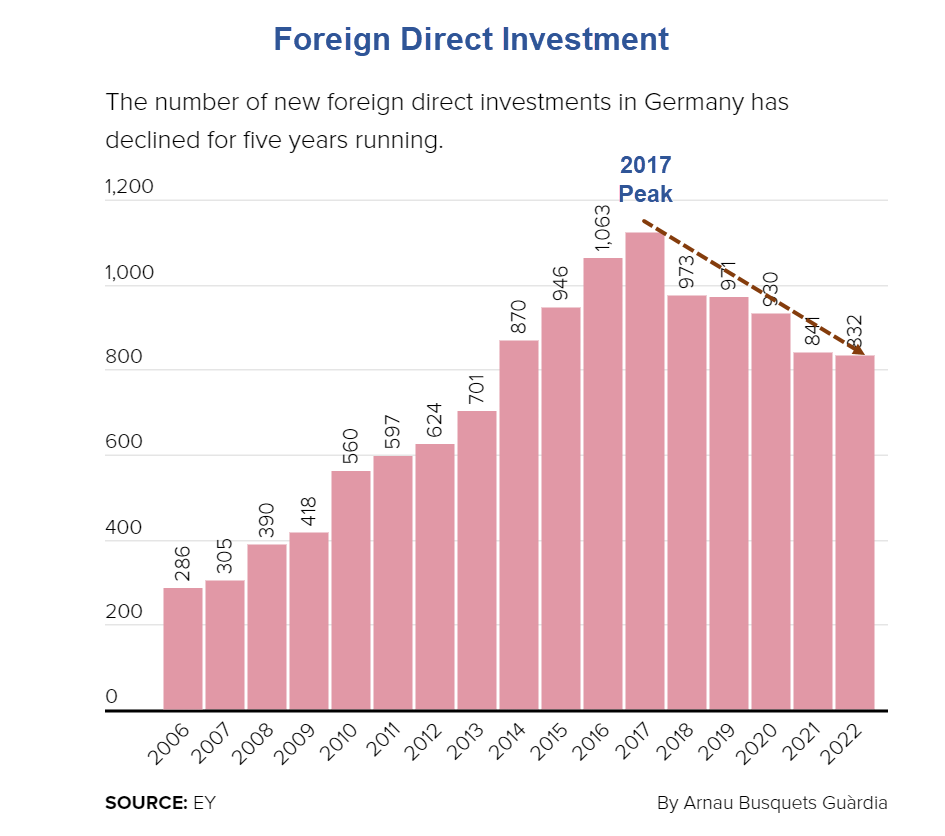

Germany's industrial production has been in decline since 2017, with factors such as the energy crisis, loss of cheap Russian gas, and competition from China contributing to the country's fading industrial competitiveness. The transition to clean energy and the scrapping of nuclear power have also impacted the economy, leading to job losses and the relocation of investments to China. Germany's lag in areas such as AI, EVs, microchips, and internet infrastructure further exacerbates its economic challenges, with the country's export prowess also diminishing.

China's industrial production and retail sales have experienced a significant jump, indicating a strong rebound in the country's economy. Industrial production rose by 6.9% in October compared to the previous year, surpassing expectations, while retail sales increased by 4.3%, marking the first positive growth this year. These figures suggest that China's economy is recovering from the impact of the COVID-19 pandemic, driven by increased consumer spending and a revival in manufacturing activities.

China's third-quarter economic growth exceeded expectations, with GDP growing at 4.9% from a year earlier, beating economists' forecast of 4.6%. Retail sales and industrial production also showed positive signs, with growth in September surpassing market expectations. However, the property sector remains a drag on the economy, and the external environment is becoming more complex. China's recovery from the COVID-19 pandemic is described as "tortuous," and consumer sentiment has been affected by the real estate debt crisis.

China's retail sales and industrial production in August exceeded expectations, with retail sales growing by 4.6% and industrial production by 4.5% compared to the previous year. However, fixed asset investment only grew by 3.2%, missing expectations, due to a decline in real estate investment and a slowdown in infrastructure investment. The Chinese government has implemented measures to support the real estate market and consumption, including a reduction in the reserve requirement ratio for banks. Moody's has downgraded its outlook on China's property sector, expecting sales to fall by around 5% in the next six to 12 months. Consumer spending remains relatively muted due to uncertainty about future income.

Germany's industrial production continues to decline, deepening concerns about the country's economic outlook. The manufacturing sector, which is heavily reliant on global trade, has been particularly affected by the ongoing trade tensions and uncertainties. This latest data adds to the gloom surrounding Germany's economy, raising fears of a potential recession.

Germany's industrial production fell 1.5% in June, driven by a 3.5% drop in the automotive sector, raising concerns of a potential recession. The construction sector also contributed to the decline. Despite emerging from a recession in the second quarter, the latest data suggests that the slight improvement may not last. The struggling car industry, accounting for 5% of the economy, is grappling with the impact of the pandemic and disrupted supply chains. While new orders in manufacturing showed some growth, the overall outlook for German industry remains challenging, with economists predicting a fall in GDP later this year.

Gold and silver prices are down due to weaker economic data from China, which has raised concerns about consumer and commercial demand for precious metals. Industrial production in China rose 5.6% YoY in April, short of market expectations for a 10.1% growth rate. Copper futures prices are also trending lower, indicating an anemic global economy. The US government could run out of money as soon as June 1. The Eurozone reported its Q1 GDP at up 0.1% from Q4 and up 1.3% YoY. The gold futures bulls have the firm overall near-term technical advantage, while the silver bulls and bears are on a level overall near-term technical playing field.

China's economic recovery from the impact of Covid restrictions remains uneven as industrial production rose by 5.6% YoY in April, lower than economists' expectations of 10.9%, while retail sales rose by 18.4%, lower than the expected surge of 21%. Fixed asset investment rose by 4.7%, against expectations of 5.5%. China stocks have pared most of the gains seen this year, and market sentiment remains weak, with Goldman Sachs economist Hui Shan expecting more measures from the government to improve market confidence.

German industrial production fell by 3.4% in March, more than expected, due to weak performance by the automotive sector, raising concerns of a recession in Europe's largest economy. The manufacture of motor vehicles and automotive parts fell by 6.5% on the previous month, while production in machinery and equipment fell by 3.4%. German industrial orders also fell by 10.7% in March, posting the largest month-on-month decline since 2020. Retail sales and exports also dropped sharply in March, increasing the odds of a downward revision to first-quarter gross domestic product.