The Euro zone is drifting towards deflation due to ongoing paralysis in fiscal policy, with Germany now experiencing significant economic slack—its GDP is 9% below pre-COVID trends—leading to deflationary pressures spreading across the region, similar to post-2008 global trends.

The euro zone economy grew by 0.2% in Q3, driven by France and Spain, despite stagnation in Germany and Italy, with the ECB likely to hold rates steady amid rising inflation and positive economic signals.

The euro zone economy grew by 0.1% in Q2, slightly better than expected, despite trade tensions and US tariffs impacting the region. Germany's economy contracted by 0.1%, indicating a slowdown, but overall resilience was observed in the euro zone amid ongoing trade uncertainties.

The European Central Bank has cut interest rates by 25 basis points to 2% and lowered its inflation expectations below the 2% target, amid a stronger euro, lower energy costs, and sluggish economic growth, as geopolitical tensions and US tariffs pose economic uncertainties.

Euro zone inflation dropped to 1.9% in May, below the ECB's 2% target, driven by declines in services inflation, which may influence upcoming interest rate decisions amid global economic uncertainties.

The European Central Bank (ECB) has cut interest rates for the first time in five years, signaling progress in reducing inflation, which has dropped from a peak of 10.6% in October 2022 to 2.6% in May. The ECB reduced its policy rates by a quarter percentage point, despite raising its inflation forecast and noting elevated wage increases. ECB President Christine Lagarde emphasized that future rate decisions will be data-dependent, and while the euro area's economic growth forecast has improved slightly, potential shocks from geopolitical conflicts could impact inflation expectations.

The European Central Bank (ECB) is expected to cut its deposit rate from 4.0% to 3.75%, marking its first rate reduction since 2019, as inflation in the euro zone has fallen closer to the ECB's 2% target. However, ECB President Christine Lagarde and other policymakers are likely to emphasize that the fight against inflation is not over, particularly with persistent price pressures in the services sector. Future rate cuts will depend on incoming economic data, and the ECB remains cautious amid signs of resilient inflation and stronger growth.

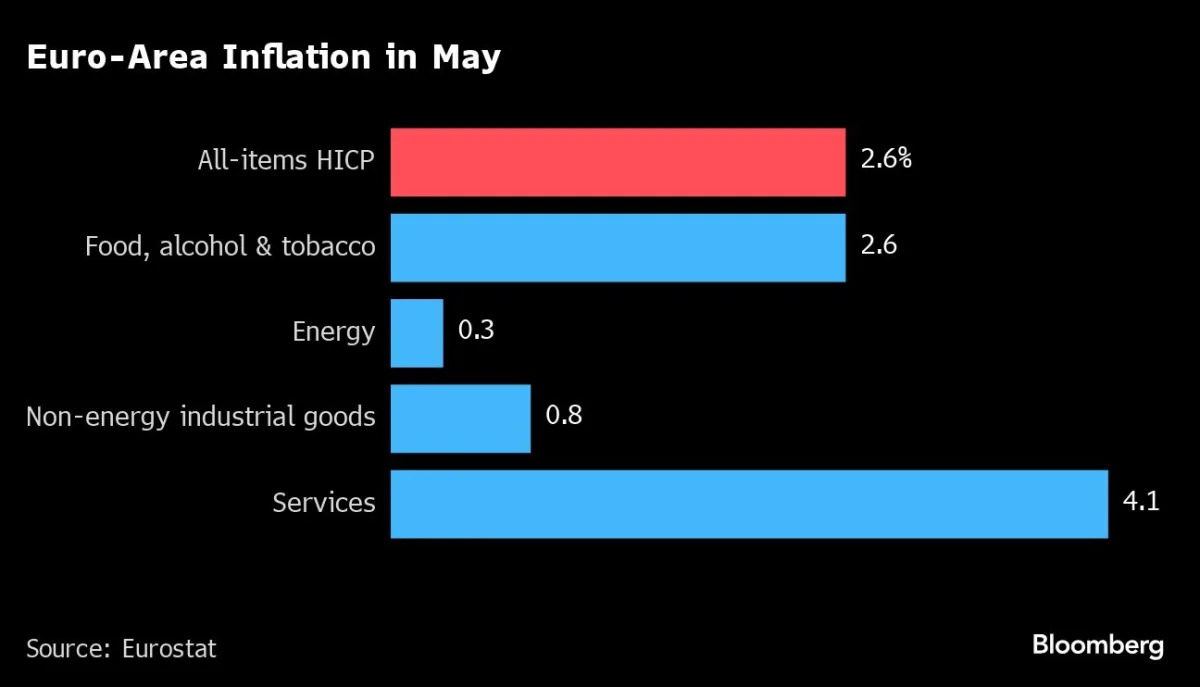

Euro-area inflation rose to 2.6% in May, surpassing expectations and complicating the European Central Bank's (ECB) planned interest rate cut next week. Despite the increase, the ECB is set to reduce the deposit rate from its current 4%, with money markets predicting two cuts this year. The rise in inflation is driven by domestic factors like wages and corporate profits, and the services sector saw a significant jump to 4.1%. ECB officials remain cautious, emphasizing a gradual approach to monetary policy adjustments.

Euro zone inflation rose to 2.6% in May, but market expectations remain firm on an interest rate cut from the European Central Bank next week. Despite the higher-than-expected inflation print, core inflation also increased slightly. The ECB is anticipated to cut rates at its June 6 meeting, marking the first reduction since 2019, with further cuts expected in 2024. The euro held steady against the U.S. dollar and British pound following the news.

The European Central Bank (ECB) has kept interest rates at record highs but hinted at a possible cut in the near future as euro zone inflation continues to decline. The ECB's decision to maintain the deposit rate at 4.0% reflects its efforts to control prices, but with inflation nearing the 2% target and economic growth stagnating, the bank is considering a rate reduction at its next meeting. ECB President Christine Lagarde is expected to address these plans and the potential for a further cut in July at her upcoming news conference.

Euro zone inflation unexpectedly slowed to 2.4% in March, with the core rate also below forecast at 2.9%, indicating potential pressure from wage growth. The European Central Bank is expected to begin lowering interest rates in June, with markets anticipating a rate cut following the release of important economic data in the coming months.

Euro zone inflation unexpectedly eased to 2.4% in March, strengthening the case for the European Central Bank to consider lowering borrowing costs from record highs. The ECB is expected to acknowledge the improved outlook at its next meeting, but policymakers are unlikely to cut rates immediately, with June being seen as the next crucial meeting for policy setting. Dovish policymakers argue that weak economic growth and corporate pricing power ease price pressures, allowing the ECB to ease up on the brakes, while most agree that the deposit rate, currently at 4%, will restrict growth until it hits 3%.

The European Central Bank held interest rates steady and reduced its inflation and growth forecasts, with projections showing a lower economic growth of 0.6% in 2024 and a decrease in inflation to an average of 2.3%. Market expectations for rate cuts have increased, with the euro trading lower against the British pound. The ECB forecasts a GDP expansion of 1.5% in 2025 and 1.6% in 2026, while Germany has slashed its growth forecast for 2024 to 0.2%. The ECB's key rate remains at 4%, and market participants are looking to the June meeting for potential rate cuts.

The European Central Bank (ECB) is locked in a battle with inflation, with rates fluctuating but showing signs of stabilizing. As the ECB prepares to release its first forecast of the year, the decision on potential policy shifts is eagerly awaited. Wages negotiations across the euro zone add complexity to the situation, with the ECB cautious about rushing to cut interest rates and risking either unchecked inflation or stifled economic growth. The differing stances of officials and the debate over the timing of potential rate cuts further complicate the ECB's strategy amidst ongoing economic and geopolitical challenges.

The OECD has raised its global growth outlook for 2024, citing an improved outlook in the United States while cutting the euro zone's forecast. The global economy is expected to ease from 3.1% in 2023 to 2.9% in 2024, better than previously expected. The U.S. economy is projected to grow 2.1% in 2024 and 1.7% in 2025, with lower inflation boosting wage growth and triggering interest rate cuts. In contrast, the euro zone's outlook has worsened, with its economy now expected to pick up from 0.5% in 2023 to only 0.6% in 2024. The OECD also anticipates rate cuts by major central banks as inflation pressures subside, with the U.S. Federal Reserve expected to move in the second quarter and the European Central Bank to follow in the third quarter.