UK interest rates are expected to remain at 4% as inflation stays high at 3.8%, with food inflation also rising, prompting policymakers to hold off on easing borrowing costs despite economic pressures.

French companies' borrowing costs have fallen below those of the government amid rising concerns over national debt, highlighting shifts in financial market dynamics.

UK government borrowing costs decreased after market nerves eased following Prime Minister's supportive comments about Chancellor Rachel Reeves, with bond yields falling and the pound rising slightly, amid ongoing concerns about fiscal discipline and political stability.

The European Central Bank is expected to maintain its deposit rate at 4% for the fifth consecutive meeting, with a potential cut anticipated in June. Economists largely agree on the decision, with only one out of 62 respondents predicting a quarter-point reduction. Investors are keenly observing for indications regarding the future policy direction beyond the initial move.

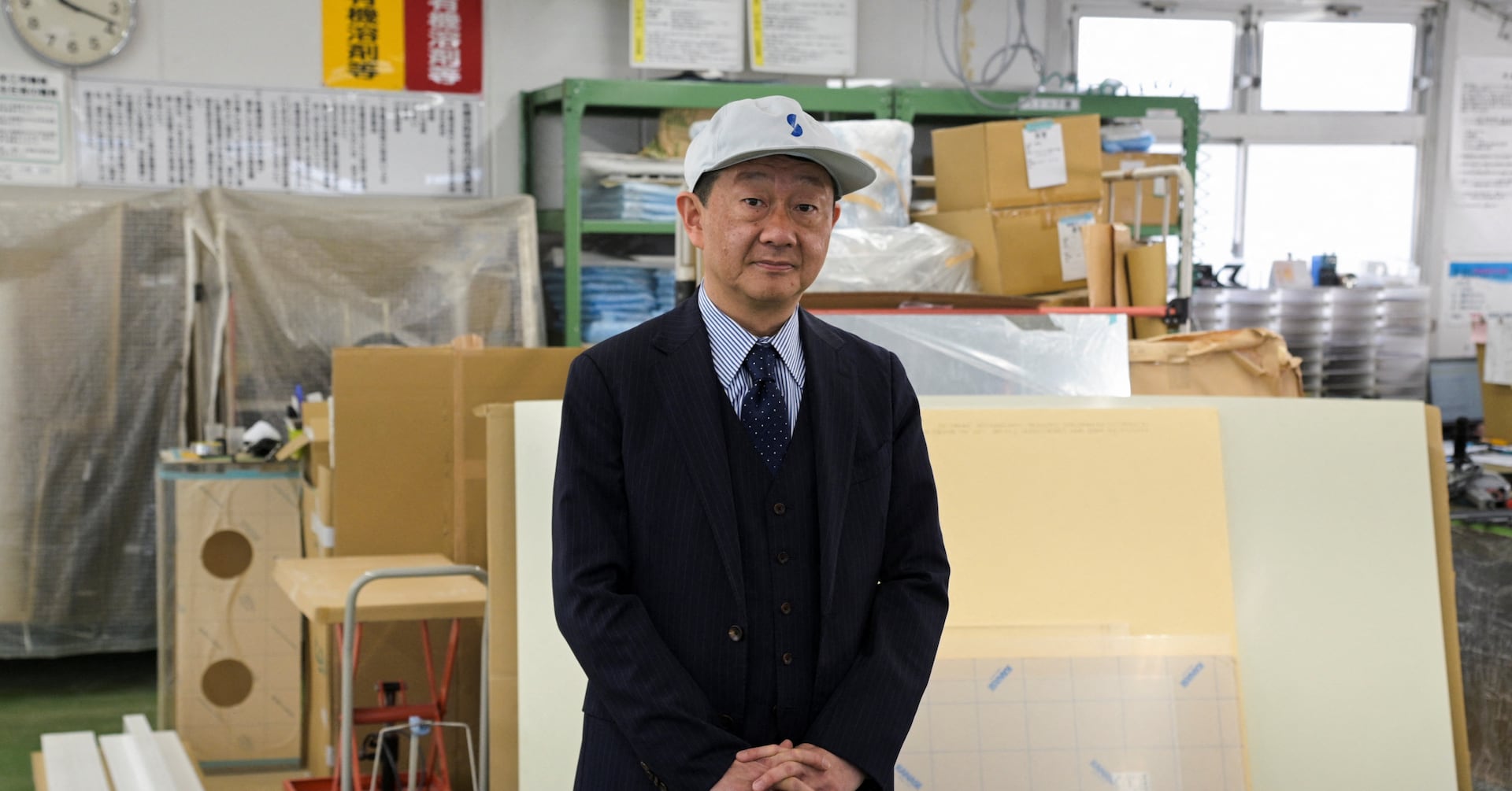

Japan's central bank raised interest rates for the first time in 17 years, prompting concerns for small business owners like Satoaki Kanoh, who worry about the impact on borrowing costs as they face the need to replace aging machinery. The shift from a deflationary mindset to adapting to higher borrowing costs poses challenges for businesses and households, with potential implications for the economy. While some hope for a stronger yen and potential salary increases, others fear lower profit margins and reduced project opportunities.

Economists expect the Federal Reserve to keep interest rates unchanged for now, despite anticipation of future rate cuts. The Fed's cautious approach aims to balance the risk of inflation and economic growth. Consumer borrowing costs remain high, with credit card rates at an all-time high and mortgage rates around 7%. While the Fed may eventually cut rates, the pace will be slow, and rates are expected to remain elevated. Savings rates have increased, offering a rare win for those building emergency funds, but there's no incentive to wait for better rates.

US households are facing increasing financial pressure due to high levels of debt, with delinquency rates on credit cards and auto loans at their highest in over a decade. The Federal Reserve's interest rate hikes have made it more expensive for consumers to borrow, leading to a significant burden on many families. The high cost of borrowing is not captured in inflation figures and is affecting consumer sentiment, potentially impacting President Joe Biden's reelection bid. Many households are struggling to make ends meet, with some blaming the current administration for the gloomy economy. The return of student loan payments is adding to borrowers' financial stress, shaping the economic outlook for many voters.

The Bank of Japan's potential move to abandon negative interest rates has raised concerns about the impact on borrowing costs and financial markets, with experts predicting that rates could rise as a result. This shift in monetary policy could have significant implications for the Japanese economy and global financial markets.

New York Community Bancorp's shares continued to plummet after receiving credit downgrades from Fitch Ratings and Moody’s Investors Service, leading to concerns about increased borrowing costs. The stock fell as much as 17% and is now trading at its lowest level since 1996. The bank's troubles began after replacing its CEO and disclosing "material weaknesses" in tracking loan risks. Despite NYCB's decline, bank stocks more broadly are performing well, with the KBW Bank Index gaining as much as 2.8% on Monday.

Deere & Co cut its 2024 profit forecast due to farmers' reluctance to make big equipment purchases amid high borrowing rates and falling crop prices, leading to a 5.4% drop in its shares. The company expects net income for fiscal 2024 to be $7.50 billion to $7.75 billion, below analysts' predictions. Demand for farm equipment is anticipated to be weaker in Central and Eastern Europe due to ongoing conflict in Ukraine and extreme weather conditions impacting crop yields. Deere plans to manage inventory levels and cut equipment production in 2024 while operating margins contracted due to lower sales of large agriculture equipment.

The Federal Reserve has decided to keep interest rates steady, signaling potential rate cuts in the future to alleviate the impact of high rates and inflation on consumers. While the pace of rate cuts is expected to be gradual, it could lead to a decrease in borrowing costs for consumers, including credit cards, mortgage rates, and auto loans. However, deposit rates may also decrease. The decision could provide relief for households struggling with high prices and credit card debt, but challenges in affordability for homebuyers may persist.

The average long-term U.S. mortgage rate has dropped to its lowest level since May, with the 30-year mortgage rate falling to 6.6% from 6.66% last week. This decline is seen as encouraging for the housing market and first-time homebuyers, although it may exacerbate the already depleted housing inventory. The decrease in rates is attributed to a pullback in the 10-year Treasury yield, and if rates continue to ease, it is expected to boost demand heading into the spring homebuying season. However, economists generally predict the average rate on a 30-year mortgage to not go lower than 6%.

Big banks are set to report fourth-quarter earnings, revealing the impact of the Federal Reserve's interest rate hikes on customer activity. Despite higher borrowing costs, households have continued to spend and borrow, while businesses have maintained healthy hiring. Major banks like JPMorgan, Wells Fargo, and Bank of America have seen strong profit growth, even after weathering challenges from smaller peers in 2023.

The Federal Reserve's forecast of potential interest rate cuts next year has sparked optimism in the stock market and relief for borrowers, as it would make loans cheaper and boost company valuations. However, savers would see a decline in income as interest rates for savings accounts decline. The anticipated rate cuts aim to reverse the recent string of rate increases that have driven up borrowing costs, benefiting consumers but not all households. While the stock market may see short-term gains, forward-looking investors have already priced in the rate cuts, limiting potential future boosts. Savers are advised to be cautious as high yields on savings accounts may decrease with a reversal in the Fed's policy.

Mortgage rates for 30-year fixed-rate loans have dropped below 7 percent, providing some relief to aspiring home buyers in the challenging housing market. The Federal Reserve's decision to hold off on raising interest rates further eases pressure on the real estate market. While borrowing costs remain higher than last year, the decline in rates has already led to an increase in mortgage applications. However, experts suggest that significant mortgage rate relief may still be months away. The widening spread between Treasury bond rates and mortgage rates is a major factor contributing to the higher borrowing costs. As the Fed is expected to cut its benchmark rate in 2024, economists anticipate that mortgage rates will continue to decrease, improving home affordability.