Russia's financial system faces increasing strain with warnings of a potential banking or nonpayment crisis due to declining energy revenues, high inflation, and rising loan defaults amid ongoing geopolitical tensions and economic challenges.

Russia's economy is currently supporting its war efforts, but it faces significant challenges ahead due to declining oil prices, potential banking crises, and consumer issues, with experts warning it could weaken further by 2026.

The article discusses how a Swiss compromise could potentially save UBS billions, highlighting the importance of strategic negotiations and regulatory considerations in maintaining financial stability.

China's major banks are facing increased pressure due to rising consumer financial difficulties, highlighting challenges within the country's banking sector.

Senator Bob Menendez was found guilty on multiple charges, with gold bars seized from his home being key evidence. The case highlights a broader trend of Americans investing in physical gold as a hedge against inflation and banking instability, with demand rising after recent bank failures. Despite the availability of gold ETFs, many prefer owning tangible gold for its perceived stability.

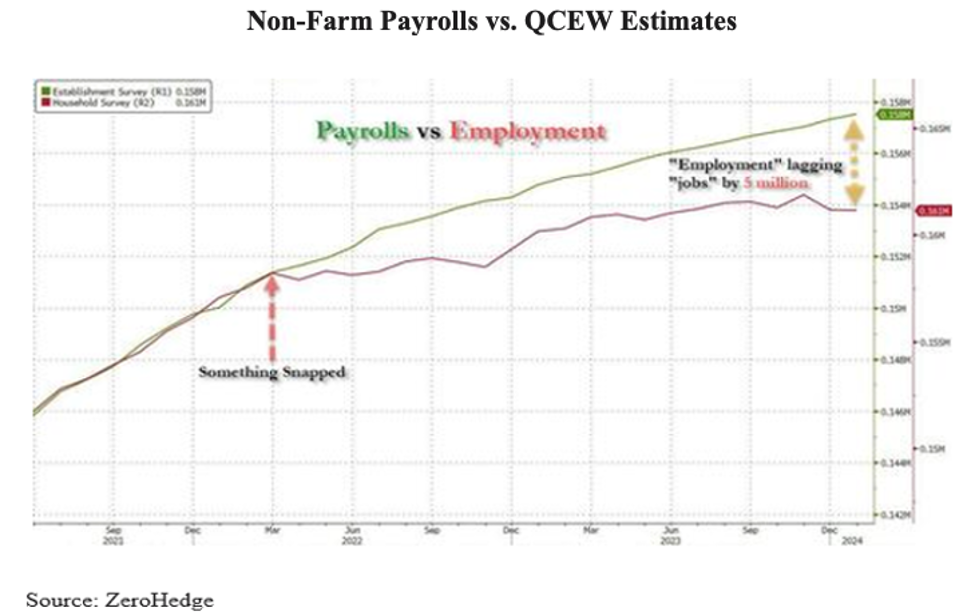

The recent employment report, while seemingly strong, has underlying issues such as disappearing full-time jobs and discrepancies between Non-Farm Payrolls and Quarterly Census of Employment and Wages data, raising questions about its reliability. Additionally, a looming commercial real estate (CRE) and banking crisis is anticipated due to rising loan delinquencies and negative equity in CRE loans, potentially leading to capital issues in the banking system. Despite the Federal Reserve's indication of higher interest rates, concerns about inflation are moderated by falling rents, prompting calls for earlier and more rapid rate cuts to address the impending challenges.

A year after its collapse and subsequent acquisition by First Citizens Bank, Silicon Valley Bank is attempting to rebuild its reputation and customer base in the tech industry. Despite efforts to reassure customers and emphasize its continued focus on start-ups, the bank has faced significant challenges in regaining trust and deposits. The bank's former dominance in the tech industry has waned, with many customers and venture capitalists now spreading their deposits across multiple banks.

New York Community Bank (NYCB) is facing pressure as its shares continue to drop due to fourth-quarter losses and lack of faith in the regional banking system, with investors reflecting on the upcoming one-year anniversary of Silicon Valley Bank's collapse. Yale Program on Financial Stability's Steven Kelly discusses the lessons learned from the 2023 banking crisis and the differences between NYCB's situation and SVB, attributing fragilities to a higher interest rate environment and market differentiation between strong and weak banks.

Bruce Van Saun, CEO of Citizens Financial Group, discusses the aftermath of the collapse of Silicon Valley Bank and the challenges faced by regional banks in the wake of the banking crisis. He attributes the failures to rapid growth, high uninsured deposits, and poor risk management. Van Saun emphasizes the joint responsibility of bank management and financial supervisors in preventing such failures. He also shares insights on the impact of the crisis on Citizens Financial Group and the changes in their business model. Additionally, he comments on New York Community Bank's situation and addresses concerns about potential banking stress related to commercial real estate loans.

New York Community Bancorp (NYCB) faces turmoil as CEO Thomas Cangemi exits, and the bank's fourth-quarter loss balloons to $2.7 billion due to a $2.4 billion goodwill impairment charge. The bank also disclosed weaknesses in its internal controls and delayed the filing of its annual report to address these issues. Alessandro DiNello, previously CEO of Flagstar Bank, has replaced Cangemi as executive chairman. The bank's troubles began a month ago when it slashed its dividend and reported a net quarterly loss, raising concerns about the regional banking world.

New York Community Bank (NYCB) has been hit with its third credit downgrade due to concerns about its exposure to commercial real estate (CRE) and a surprise loss, leading to a plunge in its stock price. The bank's management is considering selling off loans in its CRE portfolio and shrinking its balance sheet to shore up its financial strength. Treasury Secretary Janet Yellen expects additional stress and financial losses in the CRE market, while NYCB has set aside more capital to meet regulatory requirements. NYCB, which acquired failed banks during last year's regional banking crisis, has seen its stock fall over 59% in the last month.

New York Community Bank's troubles stem from acquiring billions of dollars in assets from Signature Bank during last year's banking crisis, leading to mounting losses and a steep drop in its stock price. The bank's newfound size after the acquisition forced it to keep more money on hand, affecting its profitability and prompting consideration of selling distressed assets. After a dismal earnings report, fears about the bank's ability to bear the pressure caused its stock to plummet, but a new executive chairman and turnaround plans have been announced in an effort to steer the company back to financial health.

New York Community Bancorp's stock dropped despite reassurances from its new executive chairman about the bank's strong foundation and deposit base, following a 60% decline in value and a credit rating downgrade. The bank reported increased deposits and plans to bring in new executives, but investors remained unconvinced as shares fell further. The bank's focus on reducing its exposure to commercial real estate loans amid concerns about the market's instability has raised worries of a potential banking crisis, with regulators closely monitoring the situation and expressing concerns about the impact on the banking sector.

The Federal Reserve is ending its Bank Term Funding Program, which had provided an opportunity for banks to profit from arbitrage. The program, set up during last spring’s regional banking crisis, will conclude on March 11, and new loans made before then will be at no lower than the interest rate on reserve balances. The decision comes as the program's usage reached $161.5 billion, prompting questions about its impact on regional bank stock prices and potential market sentiment.

The Federal Reserve's emergency lending program, initially launched during the 2023 banking crisis, has inadvertently become a source of easy money for banks, with borrowing from the program reaching new highs due to market expectations of multiple Fed rate cuts in the next year.