European stocks edged higher as investors awaited the ECB's interest rate decision and US inflation data, with sectors like defense and banking showing gains amid geopolitical tensions and economic concerns, while companies like Kering and Covestro moved on specific corporate news.

Global stocks declined slightly from record highs ahead of US inflation data, with markets reacting to political risks, bond yield increases, and expectations of Fed rate cuts, while the dollar weakened and oil and gold prices fell.

Asian stocks rose slightly, driven by a tech rally on Wall Street, as investors await US inflation data to gauge the Fed's rate outlook. Nvidia's earnings, despite falling short of expectations, support ongoing AI infrastructure growth. Chinese tech stocks experienced mixed movements amid warnings from Cambricon Technologies. The US dollar declined due to expectations of rate cuts, while markets also monitor upcoming US economic data and geopolitical concerns.

A $2 trillion market for inflation-linked securities in the US faces significant risk if trust in the Bureau of Labor Statistics is undermined, especially after political interference concerns following the firing of BLS chief Erika McEntarfer. Investors worry that politicization could distort CPI data, which is crucial for TIPS valuation, potentially destabilizing this market and affecting broader financial stability. The situation is compounded by recent political and economic developments, including tariffs and Federal Reserve rate expectations.

European stocks rose on bullish news in the technology sector and higher resources prices, ahead of key US inflation data. The Stoxx 600 index climbed 0.6%, driven by surging sales at Taiwan Semiconductor Manufacturing Co. and gains in miners. Tesco Plc also rose as it forecast higher retail profit and announced a share buyback, while US stock futures remained steady.

The 10-year U.S. Treasury yield saw a slight increase at the start of the second quarter, while the 2-year yield dipped marginally, with investors considering the latest U.S. inflation figures. The data, showing a 2.8% rise in the Fed's preferred inflation gauge, is likely to support the belief that the Federal Reserve will refrain from cutting rates at its upcoming meeting. Market expectations indicate a possibility of a rate cut in June, but some analysts argue for a more patient approach, while others foresee a need for more aggressive action due to a weakening job market and easing inflation.

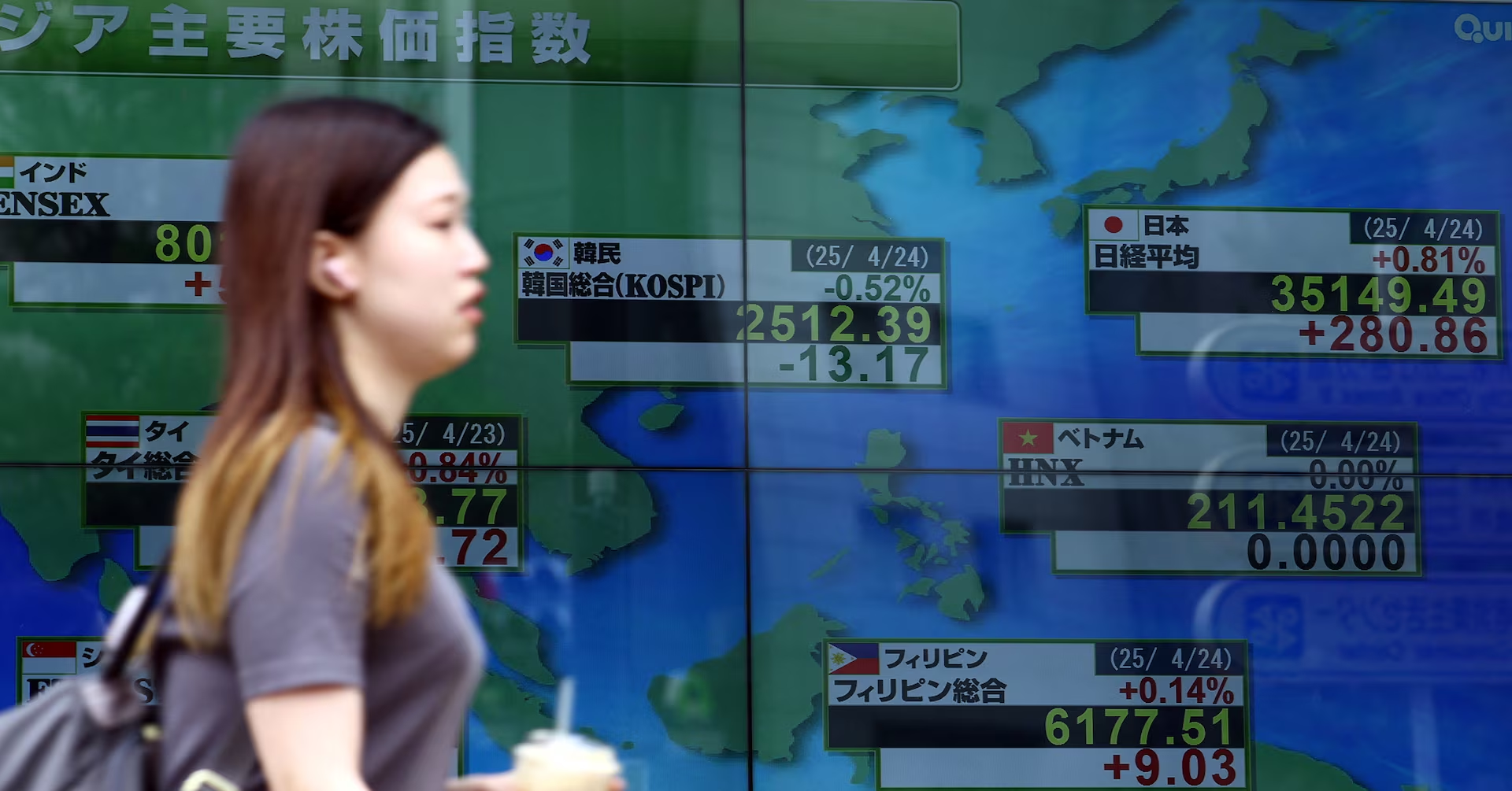

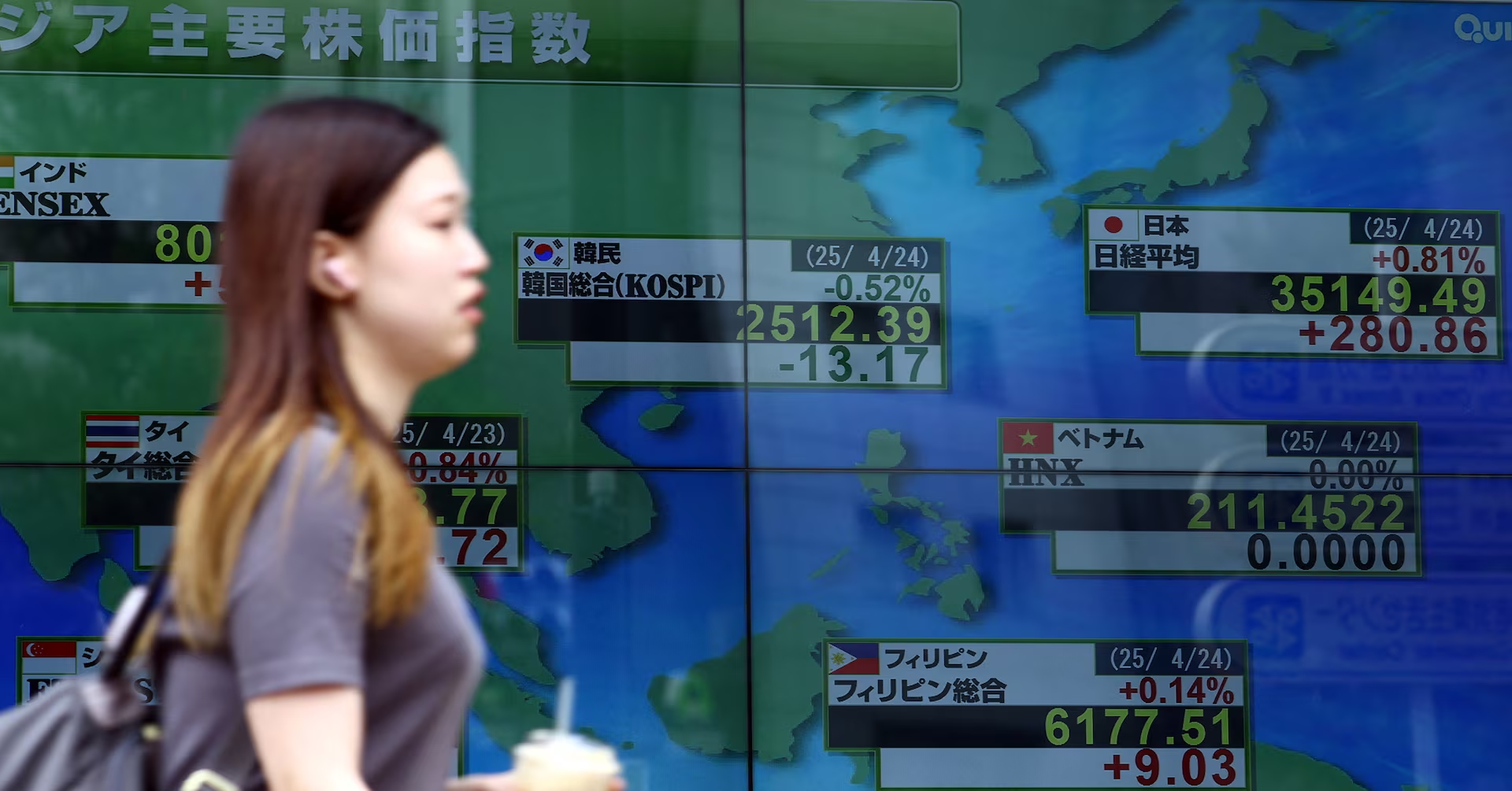

Asian stocks rose as attention turned to key US consumer price data, with markets in Japan, South Korea, and mainland China showing modest gains following a positive end to the first quarter for US stocks. Investors are awaiting the release of the Federal Reserve's preferred consumer price reading for insights into its policy outlook, while several Asian markets are closed for a public holiday. Concerns about potential swings in Japan's currency persist, and there is growing wariness of intervention. Additionally, China's corporate front saw one major property firm delaying its earnings report and another posting a historic profit decline. Swaps traders slightly trimmed wagers on a Fed rate cut, and the US government's main measures of activity posted strong advances at the end of last year. Gold hit a fresh all-time high, while oil scored a 16% quarterly gain.

Asian stocks fell as tech-led declines on Wall Street and hotter-than-forecast U.S. inflation raised concerns about the Federal Reserve cutting interest rates. U.S. benchmark bond yields neared 4.3%, the dollar rose, and crude oil prices slipped. Bitcoin retreated from an all-time high, and the U.S. Treasury bond market reacted strongly to the inflation data. The impact on equities was muted, but the tech-driven rally faced potential headwinds. Asian markets were weighed down, with Hong Kong's Hang Seng Index and South Korea's Kospi sliding over 2%. Japan's Nikkei eased 0.33%, and signs pointed to an exit from ultra-easy stimulus at the Bank of Japan's upcoming policy meeting.

In the week ahead, investors will closely watch US inflation data and retail sales for cues on potential Federal Reserve rate cuts, while Bitcoin hits record highs and oil prices remain under pressure. Wall Street faces volatility, with Nvidia's reversal and UK jobs data adding to the mix.

S&P 500 futures show mixed movement as investors await U.S. inflation data, with S&P climbing 0.2% and Nasdaq-100 adding 0.6%, while Dow Jones slips 0.1%; market assesses U.S. economy direction after hotter-than-expected consumer price index data and decline in retail sales; DoorDash shares drop on wider-than-expected loss, while Trade Desk and Applied Materials see gains; China expert calls for clearer signals on policy easing, Japan's finance minister monitors yen's moves, and BlackRock's CIO expects solid equity returns; Coinbase, Applied Materials, and Toast see significant moves in after-hours trading.

Most Asia-Pacific markets fell after U.S. inflation data sent Wall Street lower, with Hong Kong's Hang Seng index gaining, while Japan's Nikkei 225 retreated from 34-year highs. Korean Air receives EU approval for Asiana Airlines merger, and Japan's yen weakens for a seventh straight day. The Dow Jones posts its biggest one-day loss since March 2023, and oil prices rise despite stubborn U.S. inflation. All 11 sectors of the S&P 500 see losses, with real estate stocks leading the index lower.

European equity futures declined ahead of crucial US inflation data, with the Euro Stoxx 50 contract falling 0.3% and Asian markets climbing. Federal Reserve Bank of Richmond President Thomas Barkin highlighted the risk of inflation falling back toward the central bank’s target due to US businesses boosting profit margins by raising prices. Bond traders are now more in line with the Fed’s rate trajectory, but Citigroup Inc. strategists warn of overlooking the risk of rate increases following the easing cycle. In Asia, the yen fell to trade around 149 per dollar, and MSCI removed 69 companies from its China and Hong Kong global standard indexes.

Global markets are awaiting the release of US inflation data, which could impact the Federal Reserve's approach to fighting inflation. US stock-index futures and Europe’s Stoxx 600 edged higher, while bond traders are navigating well-received US debt sales and cautious language on rate cuts from central bank policy makers. In corporate news, PepsiCo Inc. shares slipped after a disappointing sales forecast, L’Oreal tumbled as Chinese shoppers reined in travel spending, and Tesco Plc advanced after Barclays Plc announced its acquisition of much of the supermarket chain’s banking business. The S&P 500 briefly hit 5,000 for the first time on Thursday before closing little changed, and the Japanese yen steadied after slipping against the greenback.

Gold prices have been consolidating without clear direction, awaiting fresh catalysts, with next week's US inflation data likely to drive market volatility and guide precious metals in the near term. The Federal Reserve's resistance to cutting rates imminently could be validated by limited progress toward disinflation in the upcoming consumer price index report. An upside surprise in the CPI numbers would be bearish for gold, while lower-than-forecast inflation readings could be positive for the yellow metal. Gold prices are currently consolidating around the 50-day moving average, with resistance at $2,065 and support at $2,005, and a breakout in either direction likely to guide the next trend.

Asia-Pacific markets, including Japan's Nikkei 225, rose ahead of U.S. inflation data, with the Nikkei briefly crossing the 35,000 mark for the first time since 1990. Investors are also awaiting the Bank of Korea's rate decision, while in the U.S., all three major indexes gained as traders anticipate the release of fresh inflation data and earnings. Additionally, analysts are discussing the performance of electric vehicle companies like Tesla and BYD, as well as offering insights on the equity market's outlook for 2024.