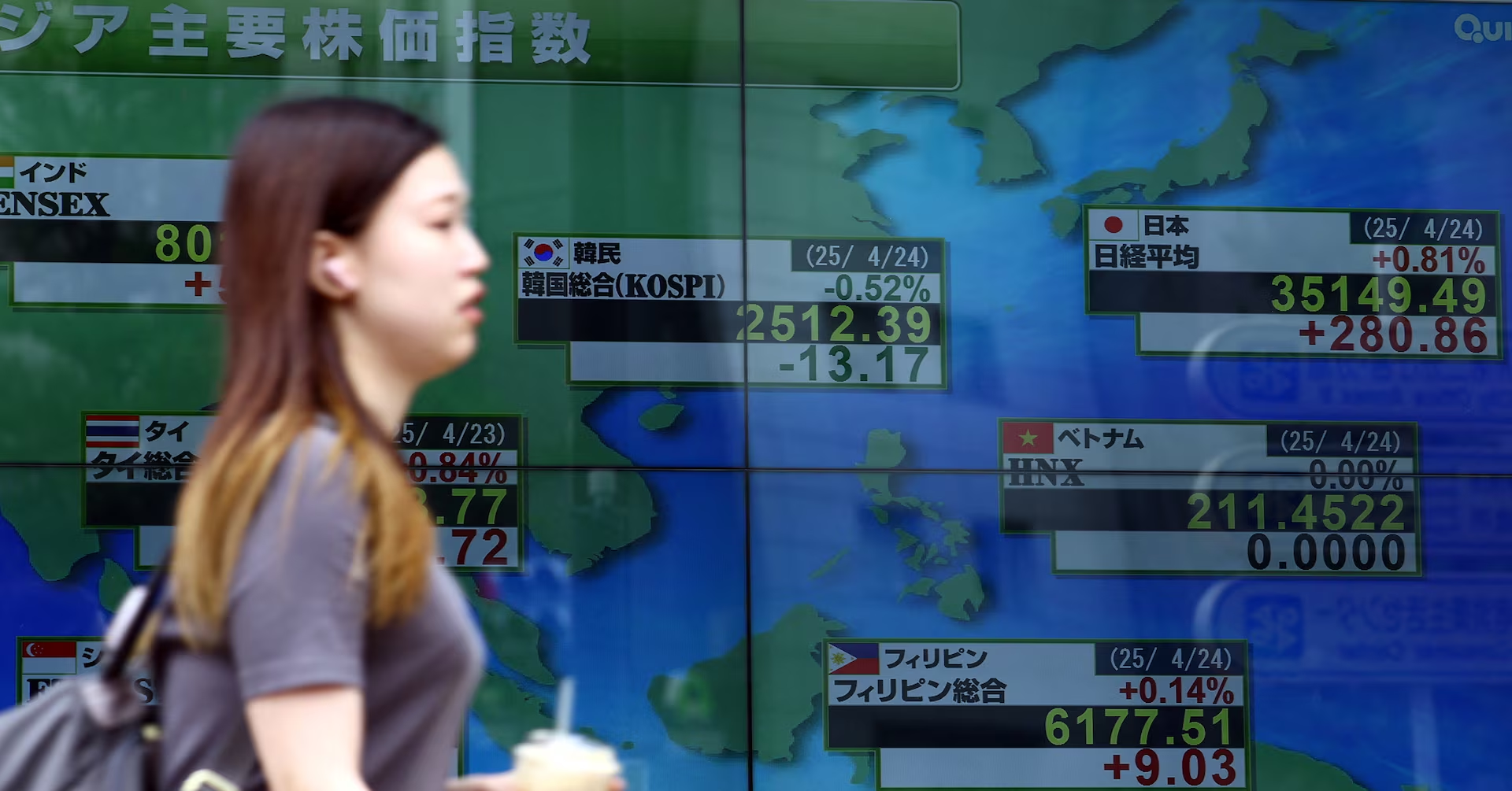

European stocks drift lower as Zelensky's Davos address dominates

European stocks are set to open modestly lower as investors digest Zelenskyy's Davos remarks and ongoing geopolitical tensions, while Trump discusses a Greenland framework and hints at a broader peace-board strategy; Ericsson announced a 15 billion krona buyback and Ubisoft warned of large losses amid restructuring, as markets await a Supreme Court ruling on Fed Governor Lisa Cook.