The article reviews top Wall Street forecasters' predictions for 2026, highlighting their accurate calls on the S&P 500's 17% rally in 2025, the market bottom after tariff-induced declines, and a significant surge in gold prices, along with their investment recommendations.

The author predicts that by 2026, market dynamics will shift with increased competition among tech giants risking the S&P 500, a rebound in the energy sector due to sentiment and demand, and benefits for housing stocks from government and Fed policies, advising a focus on high-quality energy and housing companies for better risk/reward.

Goldman Sachs CEO David Solomon is optimistic about the markets and economy, predicting a potential stock market drawdown within the next 12-24 months, a continued strong US economy in 2026 driven by fiscal stimulus and infrastructure spending, increased dealmaking, and a typical pattern of winners and losers emerging from technological booms.

Jim Cramer advises investors to stay the course and invest at least $50 a month, starting with an S&P fund, despite upcoming economic challenges and inflation concerns, emphasizing the importance of long-term commitment and resilience in the market.

Cantor Fitzgerald CEO Howard Lutnick warns of a "very ugly" real estate market in the next 18 months to two years, predicting a "generational" shift and massive defaults of $700 billion to $1 trillion in loans. He anticipates commercial loan defaults due to high rates, leading to a significant impact on real estate equity. Lutnick also cautions that people are "overly optimistic" about the Federal Reserve and future rate hikes, suggesting that rates will likely remain steady.

CNBC's Jim Cramer predicts a potential sector rotation out of tech stocks in 2024, as investors may start favoring undervalued sectors like food or pharmaceuticals. He advises taking profits from high-performing tech stocks and investing in companies with solid leadership and reasonable valuations. Cramer also emphasizes the influence of the Federal Reserve's decisions on the market, suggesting that investors wait for a sell-off before buying.

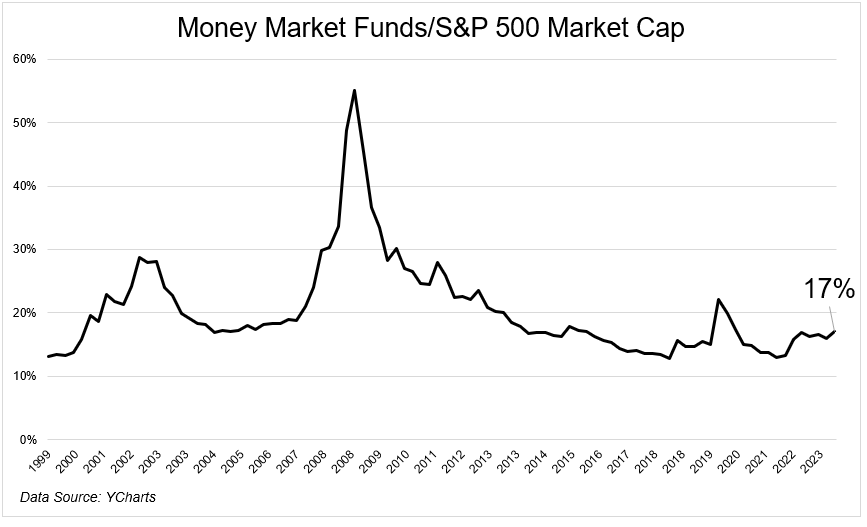

The Irrelevant Investor shares ten predictions for 2024, emphasizing the unpredictability and educational value of such forecasts. Predictions include no consolidation in media/streamers, Apple being replaced by Netflix in the "magnificent 7," Amazon's stock gaining over 25%, Microsoft reaching a $4 trillion market cap, and Robinhood being acquired. Other forecasts involve money remaining in money market funds, inflation hitting the Fed's target, an economic overheating, a "vibecovery" beginning, no recession with stocks gaining 20%, and Bitcoin reaching $100k. The author acknowledges the likelihood of something unexpected rendering many predictions obsolete and encourages readers to make their own predictions as a learning exercise.

Industry analysts predict that the S&P 500 will close above 5,000 at the end of 2024, with a bottom-up target price estimate of 5,068.41. However, historical data shows that analysts have historically overestimated the closing price of the index by an average of 7.2% one year in advance. Applying this average, the expected closing value for 2024 would be 4,705.21, which is 2.6% above the current closing price.

Economists and investors are divided on when a recession might occur, with some predicting early next year and others suggesting a synchronized global downturn in 2024. The stock market has shown little sign of an impending downturn, with small-cap stocks performing well and the consumer discretionary sector propped up by strong economic data. However, the bond market tells a different story, with the New York Federal Reserve's recession probability model indicating a 71% chance of a recession by May 2024. The uncertainty is due to unique factors such as the pandemic, stimulus spending, and the Federal Reserve's interest rate hikes, leaving markets unsure of what to expect. Additionally, the emergence of El Niño could pose a threat to the US economy, potentially leading to extreme weather events and increased costs for food and the airline industry.

Bond traders continue to doubt the Federal Reserve's commitment to its inflation fight into 2024, despite the odds of a quarter-point increase in the federal-funds target becoming a near lock at the Fed's policy meeting on May 2-3. Markets keep pricing in rate reductions in 2023's second half, contrary to the best guesses of Fed Chairman Jerome Powell and his colleagues that the key policy rate will end the year at 5.1%, which implies no cuts after the May hike.