February’s stock selloff was driven by AI-related fears and private-credit stress, with lenders such as Blue Owl and Apollo Global Management facing withdrawals and asset evaluations that spooked investors. Inflation signals and a rush to safer assets boosted bonds and haven metals, leaving major indexes lower for the month even as the Dow posted a monthly gain.

Jamie Dimon warns at an investor event that the opaque $3 trillion private-credit market harbors 'dumb stuff' risks that could spark a crisis like 2008, as AI-fueled private lending outpaces transparency; Fed minutes flag vulnerabilities in private credit despite low public spreads, highlighting a potential risk blind spot in the financial system.

A speculative Substack piece from Citrini Research envisions AI agents triggering a 2027–28 downturn: mass white‑collar unemployment, disruption of software and middlemen businesses, a wave of private‑credit defaults and a mortgage crisis, and a 57% S&P crash accompanied by Occupy Silicon Valley protests. While many analysts chalk it up to sensationalism, the scenario raises questions about how AI could reshape demand, jobs, and policy responses in a real economy.

Blue Owl Capital’s decision to accelerate investor returns by selling loan assets from a private fund has traders worried about liquidity in the rapidly grown, opaque private-credit market. The sector, funded by pension funds and other institutions and lightly regulated, has surged since 2008, making the move appear routine to some but a potential warning sign to others. The episode underscores concerns about retail investors in semiliquid private-credit products and the risk of spillovers to broader financial markets, even as Blue Owl and peers push back on claims of a liquidity freeze.

Investors dumped asset-manager stocks last week after concerns about Blue Owl Capital’s private‑credit fund sparked fears of liquidity strain and possible spillovers to other private‑debt lenders and BDCs, prompting worries about how quickly portfolios could be exited and at what prices. While analysts say private credit has grown large and isn’t yet a systemic crisis, the episode highlights liquidity risk in publicly traded vehicles that hold private loans and the sensitivity of the asset-management sector to private‑debt conditions.

Blue Owl Capital reportedly sold a $1.4 billion portfolio of loans at about par (99.7%) to major pension funds and its own insurer to raise cash for private-credit redemptions.

Blue Owl Capital said it would stop offering a fixed quarterly redemption amount for one fund and instead determine payouts, accelerating returns; it also disclosed a $1.4 billion loan sale with about $600 million to be returned to investors, a move that triggered a stock slide and raised concerns about liquidity and risk in the private-credit industry as peers slipped and analysts warned of potential hidden vulnerabilities outside traditional banking.

CVC agreed to acquire Marathon Asset Management for up to $1.2 billion in a cash-and-equity deal to expand its US credit capabilities and broaden its multi-asset credit platform. The base consideration is $400 million in cash and up to 45 million SubCo Units exchangeable for CVC shares, plus up to $800 million in CVC equity, with earn-outs of up to $200 million cash and $200 million in SubCo Units. Marathon’s minority partner will receive $280 million in cash. The deal is expected to close in Q3 2026 and be EPS neutral in 2027 and accretive from 2028. Marathon will be rebranded CVC-Marathon, with co-heads Bruce Richards and Lou Hanover leading the combined credit business. Post-close, CVC’s Fee-Paying AUM is targeted at about €61 billion, supporting plans to reach €200 billion by 2028 across Private and Public Credit and multiple client channels.

Leuthold Group warns that the convergence of AI, bitcoin and private credit forms a largely underappreciated market threat, signaling higher volatility and potential cross-asset stress as these themes intertwine. The firm has cut its tech exposure and shifted toward financials and healthcare, favoring big banks (JPM, Morgan Stanley), biotech/pharma, and gold miners, while steering clear of regional banks and consumer lenders. They also flag a crypto-financing link that could spark liquidity issues if bitcoin prices slide, with yield-curve dynamics seen as a tailwind for banks.

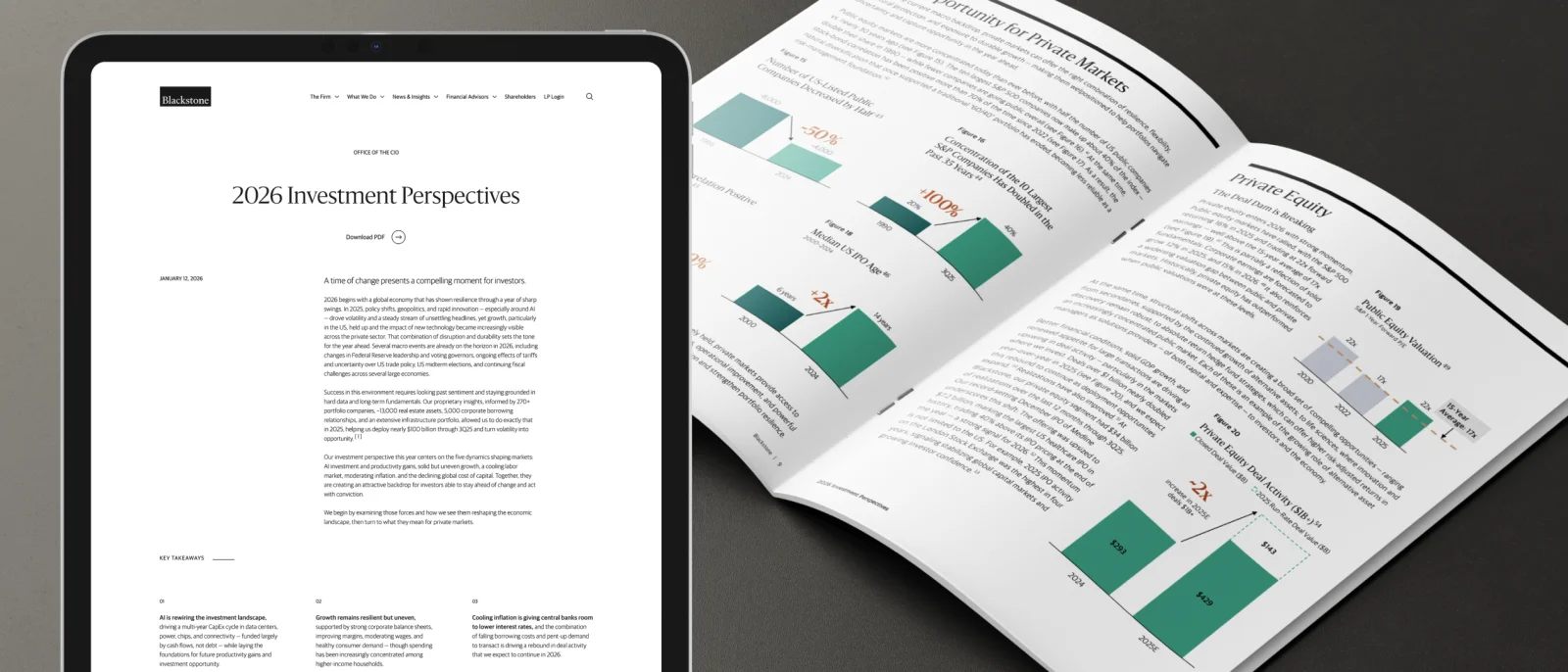

Blackstone’s 2026 Investment Perspectives argue that AI-driven productivity, moderating inflation, and cheaper capital underpin a multi-year expansion in private markets across private equity, real estate, credit, and infrastructure. AI is driving a significant CapEx cycle in data centers, chips, and digital infrastructure funded largely from cash flow, with growth being resilient but uneven as labor markets cool. A rebound in deal activity and exits, aided by lower financing costs, supports a cyclical upswing; real estate is in early recovery, private credit offers durable income with downside protection, and infrastructure demand remains strong from energy transition and AI needs. International markets show opportunity in India and Japan, with Europe offering selective bets. Blackstone stresses disciplined underwriting, data-driven insights, and platform scale to capitalize in 2026.

Morgan Stanley promoted 184 new managing directors for 2026, highlighting a strong AI leadership track with several AI-focused appointees, plus hires in private credit, investment banking, trading, and sales (including biotech banking and ex-hedge fund traders). Base MD pay is about $400k with additional bonuses, and the list features promotions across regions and functions, with names listed at the article’s end.

The article discusses the resurgence of traditional banks in the lending market as regulatory restrictions ease, allowing them to compete more effectively against private credit firms, which have previously gained an edge. Major banks like JPMorgan and Wells Fargo are expanding their loan portfolios, narrowing the gap with alternative asset managers, amid a shifting regulatory landscape and industry rivalry.

Ares Management is considering acquiring a large private equity firm to expand its leveraged buyout business and compete with industry giants, driven by the growing interest in private assets among US retirement plans. The company aims to manage at least $775 billion in assets within three years and is exploring strategic acquisitions to bolster its private equity segment, which currently represents a small portion of its assets. Despite no imminent deals, Ares is positioning itself for growth through potential acquisitions and strategic investments.

Treasury Secretary Scott Bessent plans to advocate for a new rule requiring regional Federal Reserve presidents to have lived in their district for at least three years, aiming to ensure local representation and address concerns about the Fed's mission creep and complexity. He also discussed the role of the Fed's balance sheet and concerns over private credit growth.

Investments in alternatives are projected to reach $32 trillion by 2030, driven mainly by wealthy investors such as ultra-high-net-worth individuals and family offices, with private equity and private credit expected to see significant growth amid a recovering market and AI boom, despite recent declines in institutional fundraising.