The US core consumer price index, excluding food and energy costs, rose 0.4% from February and 3.8% from a year ago, potentially delaying any Federal Reserve interest-rate cuts as inflation continues to exceed forecasts.

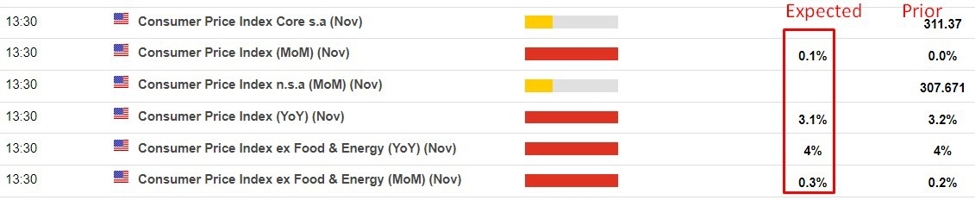

Inflation in the US declined slightly in November 2023, with the consumer price index (CPI) increasing by 3.1% from the previous year, down from 3.2% in October. Gasoline prices were a major contributor to falling inflation, dropping 6% in November. The core CPI, which excludes volatile energy and food prices, remained flat at an annual rate of 4%. Shelter inflation, the largest household expense, decreased slightly in November. Economists expect inflation to continue to decrease heading into 2024, driven by disinflationary pressures in the system. The Federal Reserve aims for a 2% annual inflation rate over the long term.

Inflation in the US slowed to a 3.1% annual rate in November, in line with expectations, as prices for goods and services increased 0.1% for the month. The core Consumer Price Index (CPI), which excludes volatile food and energy prices, rose 0.3% on the month and 4% from a year ago. The November numbers are still above the Federal Reserve's 2% target, but show progress. The Fed is expected to hold interest rates steady during its two-day policy meeting, signaling that the policy tightening is over and future cuts are likely.

The upcoming US inflation data for November, specifically the Core CPI, could impact future rate cut timing as markets will be watching for any unexpected rise above expectations. If the data comes in above the upper end of estimates, ongoing pricing pressures will likely influence the timing of rate cuts. Conversely, if the data falls below the lower range of estimates, it could have the opposite effect.

UK inflation dropped to a two-year low of 4.6% in October, down from 6.7% the previous month. The headline consumer price index remained flat on a monthly basis, contrary to expectations of a slight increase. Core CPI, which excludes volatile items, also decreased to 5.7% annually. The drop in inflation was primarily driven by housing and household services, as well as food and non-alcoholic beverages. The Bank of England is likely to keep interest rates unchanged in December, and further declines in inflation may bring it closer to the central bank's 2% target.

Inflation in the US declined in October as gasoline prices retreated, but economists warn that price pressures remain and it may take time for them to return to pre-pandemic levels. The consumer price index increased by 3.2% from a year earlier, down from 3.7% in September. Gasoline prices dropped 5% in October, contributing to the overall decline in inflation. However, underlying inflation trends, excluding volatile energy and food prices, showed a decrease in the core CPI to an annual rate of 4%. Housing costs, the largest expense for households, have moderated, but food inflation increased slightly. Other categories with notable increases include motor vehicle insurance, recreation, personal care, and household furnishings and operations.

US consumer prices rose modestly in June, with the consumer price index (CPI) increasing by 0.2% and the core CPI (excluding food and energy) also gaining 0.2%. The year-on-year CPI climbed 3.0%, the smallest rise since March 2021, while the core CPI rose 4.8%, the smallest gain since October 2021. The slowdown in underlying inflation has led to speculation that the Federal Reserve may pause its interest rate hikes. However, inflation remains above the Fed's 2% target, and the labor market remains tight.

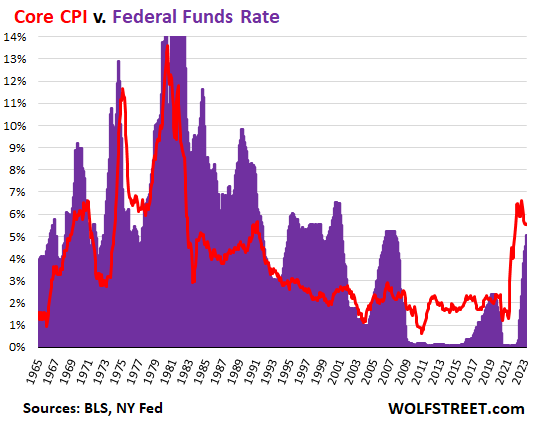

The Fed's policy rates have been raised by 500 basis points in a little over a year, but "core" CPI, which excludes the volatile food and energy components, has gotten stuck at around 5.5% to 5.7% for the fifth month in a row. Negative real policy rates are still a form of interest rate repression, and are still stimulative of the economy and of inflation. The crybabies on Wall Street are out there in force screaming about those unfair interest rates and clamoring for immediate rate cuts, like in June, to remove this incredible injustice of 5% short-term rates and even lower long-term Treasury yields (the 10-year Treasury yield is at 3.43%, LOL), when core CPI is 5.5%.