Investors are increasingly viewing large corporations like Microsoft and Airbus as safer investments than governments due to rising sovereign debt, fiscal backsliding, and erosion of the perceived rule of law, leading to a shift in bond market dynamics where corporate bonds often offer lower yields than government bonds.

EA's planned $55 billion sale to Saudi Arabia and private equity faces concerns over credit downgrades, risky AI investments, and potential impacts on studio staff and inclusivity, amid a shifting regulatory and political landscape.

Egan-Jones Ratings Co., a small but influential credit rating agency, has grown rapidly by providing private credit ratings that are widely used in the industry, especially by insurers seeking higher yields. Despite its success, the firm faces scrutiny over the accuracy and potential conflicts of interest in its ratings, which have sometimes been overly optimistic and led to defaults. Regulatory and industry concerns highlight the risks of relying on private, less transparent ratings in a rapidly expanding market, raising questions about the true safety of private credit investments.

Moody's warns of further economic pain following a surge in corporate defaults, indicating a challenging financial outlook. The credit rating agency's assessment suggests that the economic impact of the pandemic is far from over, with corporate defaults likely to continue posing significant challenges in the near future.

Moody's has issued downgrade warnings for the US and China, the world's two largest economies, citing concerns over rising debt levels and economic challenges. Turkey, on the other hand, could see its first credit rating upgrade in over a decade if it maintains its policy repair efforts and attracts foreign investors. Oman may be elevated to investment-grade status, potentially leading to significant inflows and lower borrowing costs. Panama faces the risk of being downgraded to "junk" status due to the closure of a major copper mine. Israel's ongoing conflict with Hamas could result in its first-ever credit rating cut. Overall, 2024 is expected to bring pivotal moves in sovereign credit ratings due to record debts, higher borrowing costs, and geopolitical tensions.

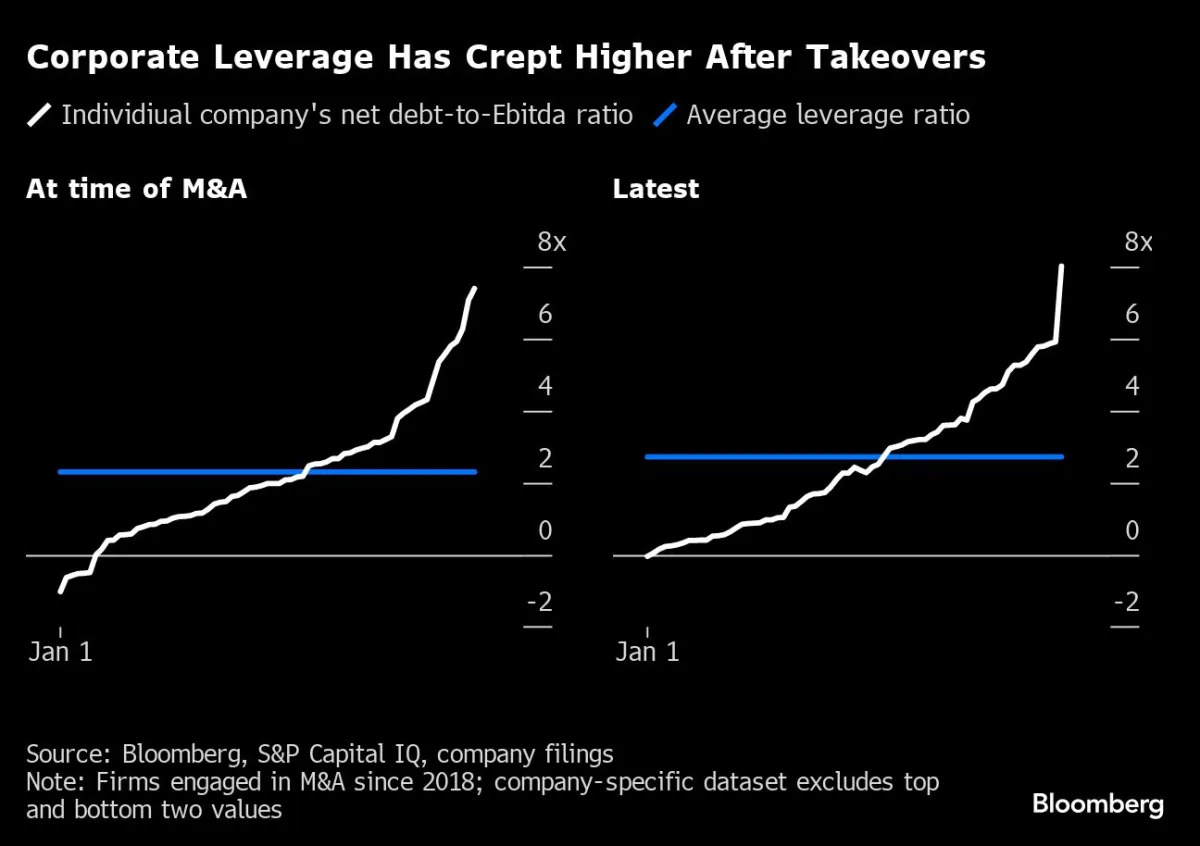

Companies that relied on cheap credit to fund large mergers and acquisitions (M&A) during the boom times are now facing challenges in delivering on their promises and servicing their debt loads in a new environment of higher interest rates and weakening consumer demand. An analysis of 75 of the largest corporate acquisitions over the past five years, totaling nearly $1.3 trillion, reveals that less than half of the companies have managed to reduce leverage ratios since their acquisitions. Almost a third of the firms now have leverage ratios above 3.5, compared to 16 at the time of the acquisitions. The need to refinance debt and deliver on synergies or earnings growth is becoming a concern, especially as cash buffers erode, sales decline, and the risk of recession looms. Companies such as Walgreens, Rogers Communications, and International Flavors & Fragrances have seen their creditworthiness slide, while others, like Warner Bros. Discovery and SAP, continue to seek smaller bolt-on acquisitions. However, caution is advised as higher interest rates may lead to downgrades and mistakes in dealmaking.

Wall Street is concerned that the U.S. could lose its last AAA credit rating due to political chaos and the potential for another government shutdown. The U.S. has already faced downgrades in the past, and Moody's warned that a shutdown would be a credit negative for the country. The sustainability of U.S. debt is less of a focus for credit-rating firms than dysfunction in the decision-making process of elected officials. While a third downgrade would be an unpleasant event, the market's memory of it would likely be short. The rising Treasury yields are also causing concern in the financial markets.

Fitch Ratings has warned that US banking giants, including JPMorgan, could face ratings reassessments if the overall industry's score is downgraded. In June, Fitch lowered its "operating environment" score for US banks, and another downgrade could lead to negative rating actions for more than 70 US banks. The restrictive monetary policy imposed by the Federal Reserve has created a challenging environment for banks, and Moody's has already slashed credit ratings for 10 US banks. The potential downgrades could have consequences for industry leaders and smaller lenders alike.

Moody's credit rating cuts have put additional pressure on regional bank stocks, which have already been underperforming this year. However, some analysts believe that there are bargains to be found in the sector. Wells Fargo banking analyst Michael Mayo suggests that the price discount on regional bank stocks due to rising interest rates and potential recession fears is overblown. He advises investors to look for consistency of strategy and management, credit quality, cost control, and sound capital levels when considering regional bank investments. Analysts recommend stocks such as PNC Financial Services, U.S. Bancorp, Fifth Third Bancorp, East West Bancorp, New York Community Bank, and Columbia Banking System as potential opportunities in the regional bank sector.

The Dow Jones Industrial Average dropped nearly 400 points after Moody's downgraded the credit ratings of several smaller and midsized banks, raising concerns about their financial strength. This decline in bank stocks, along with mixed earnings reports and worries about China's economy, contributed to a broader slump in global financial markets. Additionally, the upcoming release of data on job openings and inflation in the US could further impact market sentiment. The Federal Reserve's decision to raise interest rates has also affected banks, leading to reduced profits and devalued investments.

Moody's has downgraded the credit ratings of 10 US banks and placed several major lenders on review for potential downgrades, citing growing profitability pressures and the looming possibility of a mild recession. The agency also changed its outlook to negative for several major lenders, including Capital One, Citizens Financial, and Fifth Third Bancorp. The downgraded banks include M&T Bank, Pinnacle Financial Partners, Prosperity Bank, and BOK Financial Corp. Moody's assessment changes affect a total of 27 banks in the sector.

Moody's has downgraded the credit ratings of several small to mid-sized US banks and warned of possible downgrades for some of the nation's largest lenders, citing funding risks and weaker profitability. The agency highlighted growing profitability pressures and a potential decline in asset quality, particularly in commercial real estate portfolios. Moody's also changed its outlook to negative for eleven major lenders. The report comes amid tightening monetary conditions and concerns over a potential recession, as well as tighter credit standards and weaker loan demand reported by US banks in the second quarter.

Moody's has downgraded credit ratings for 10 small and midsize US banks and warned of potential downgrades for major lenders, including U.S. Bancorp, Bank of New York Mellon Corp., State Street Corp., and Truist Financial Corp., due to mounting funding costs and risks associated with commercial real estate loans amid weakening demand for office space. Rising interest rates are increasing the cost of funding for banks, eroding their asset values and making it harder for commercial real estate borrowers to refinance their debts. Moody's also highlighted potential regulatory capital weaknesses and declining profitability as factors contributing to the review.

As the US approaches its debt limit, credit-rating companies Moody's, Fitch Ratings, and S&P Global Ratings are holding steady on the country's top rating, assuming a deal will be struck to avoid default. However, repeated political tussles are eroding the stability and predictability that support Washington's status as the risk-free standard in world financial markets. While none of the raters have downgraded the US since S&P did so in 2011, the country's credit rating would likely suffer another blow if Congress can't reach an agreement in time.

Moody's has downgraded the credit ratings of First Republic Bank due to the bank's deteriorating financial profile and challenges faced by the lender due to increased reliance on funding amid deposit outflows. The agency cut the bank's long-term issuer rating and local currency subordinate ratings to B2 from Baa1 and long-term local currency bank deposit rating to Baa3 from A1, among others. Moody's believes the bank's high cost of borrowings and the high proportion of fixed rate assets at the bank is likely to have a large negative impact on First Republic's core profitability in coming quarters.