With the Federal Reserve expected to cut rates next week, now is a good time to lock in high-yield CDs, such as OMB Bank's 4.36% APY for a 3-month term, to secure a guaranteed return before rates fall further.

Despite a slight decrease in average CD yields to 1.75%, some banks and credit unions are offering very high APYs, with California Coast Credit Union providing up to 9.5% APY on a 5-month certificate, though with deposit and membership restrictions. The Federal Reserve's hold on interest rates suggests CD yields will remain stable for now, making locking in high rates a prudent choice for low-risk investors. The article details the top CD rates available in June 2025, including accessible options with lower minimum deposits and broader eligibility.

Experts recommend five strategies for investing in certificates of deposit (CDs) to maximize returns: shopping around for the best rates, choosing CD terms based on liquidity needs, creating a CD ladder, purchasing long-term CDs to lock in rates, and reinvesting proceeds from matured CDs. These strategies can help optimize CD investments in the current high-rate environment, though it's also important to diversify assets.

Online-only personal savings accounts offer the highest interest rates, beating traditional accounts and even one-year CDs, while credit union checking accounts have significantly higher rates and lower fees compared to regional banks. Credit unions also offer the best CD rates across all maturities, while business accounts are the most expensive and offer the lowest rates. Overall, electronic statements are recommended to save money, and students can benefit from checking accounts with the lowest fees.

Certificate of deposit (CD) rates have remained relatively stable, with the national average for a 6-month CD at 1.76% and a 1-year CD at 1.92%. The top national rate for a 6-month CD is 5.50%, while the highest national rate for a 12-month CD is 5.37%. Rates for longer-term CDs, such as two-year and three-year CDs, have also remained steady. It's important to note that CD rates change regularly, and individuals are encouraged to seek personalized financial advice before making any investment decisions.

Today's certificates of deposit offer higher rates than the FDIC national average, with some digital banks and online accounts offering over 5.05% APY on terms of 10 months or longer. The Federal Reserve's recent decision to maintain the federal funds target interest rate has left uncertainty about potential rate cuts, as inflation remains a concern. CD rates are influenced by the Federal Reserve's key interest rate, and the latest data shows steady or increasing rates on most terms. CDs offer guaranteed returns and higher rates than traditional accounts, but come with penalties for early withdrawals. Alternatives include high-yield savings accounts, money market accounts, and bonds.

Financial experts have varying predictions for CD account interest rates in spring 2024. Some anticipate further rises, while others expect rates to remain steady or drop later in the year due to potential Federal Reserve interest rate cuts. It's advised to consider foreseeable expenses and choose a CD term aligned with specific savings goals, as higher rates are currently available but accessibility to funds may be limited.

Following the latest inflation report, CD rates are high and likely to stay elevated for the short term, making it a great time to open a certificate of deposit (CD) account. With inflation at 3.1% year over year, borrowers may not see relief in interest rates anytime soon, making it beneficial for savers to lock in higher rates with a CD account. CD rates are currently offering around 6% or higher, providing a significant opportunity for increased earnings on savings compared to regular or high-yield savings accounts.

The top 10 CD rates for February 2024 are at high levels, with some exceeding a 6% annual percentage yield (APY). However, experts warn that rates could begin falling in the next few months due to potential Fed interest rate cuts. Despite this, the average deposit rate for a 12-month CD has increased significantly over the past year. Various credit unions offer high APYs, but many have membership requirements. For those seeking accessible options, banks like CIBC Bank USA and BMO Alto offer competitive rates with minimal requirements.

The Federal Reserve's pause on rate hikes has led to banks and financial institutions offering high annual percentage yields (APYs) on certificates of deposit (CDs), particularly for 1-year CDs. Some of the best 1-year CD rates for February 2024 include Resource One Credit Union at 6.17% APY, Lafayette Federal Credit Union at 5.56% APY, and Salem Five at 5.55% APY. Locking in a 1-year CD now could provide some of the best rates available on interest-bearing accounts and guarantee returns for the full CD term.

The Federal Reserve's rate hikes have led to a situation where short-term CDs offer higher yields compared to longer-term ones, a reversal of the typical scenario. With the possibility of the Fed cutting rates in 2024, experts anticipate a decline in CD rates overall, with short-term rates likely to remain more competitive. Despite this, locking in a long-term CD now could still be beneficial for savers, as it would secure a higher rate for a longer period, although early withdrawal penalties should be considered.

The Federal Reserve's recent 11-hike cycle has left the federal funds rate at 5.33%, resulting in higher short-term CD rates due to economic uncertainty and the Fed's response to inflation. Experts suggest that the traditional model where long-term CDs offer higher rates than short-term ones could return as economic stability is restored, but the timing of this shift is uncertain and dependent on various factors. Opening a CD now may be advantageous to lock in an elevated interest rate before rates drop.

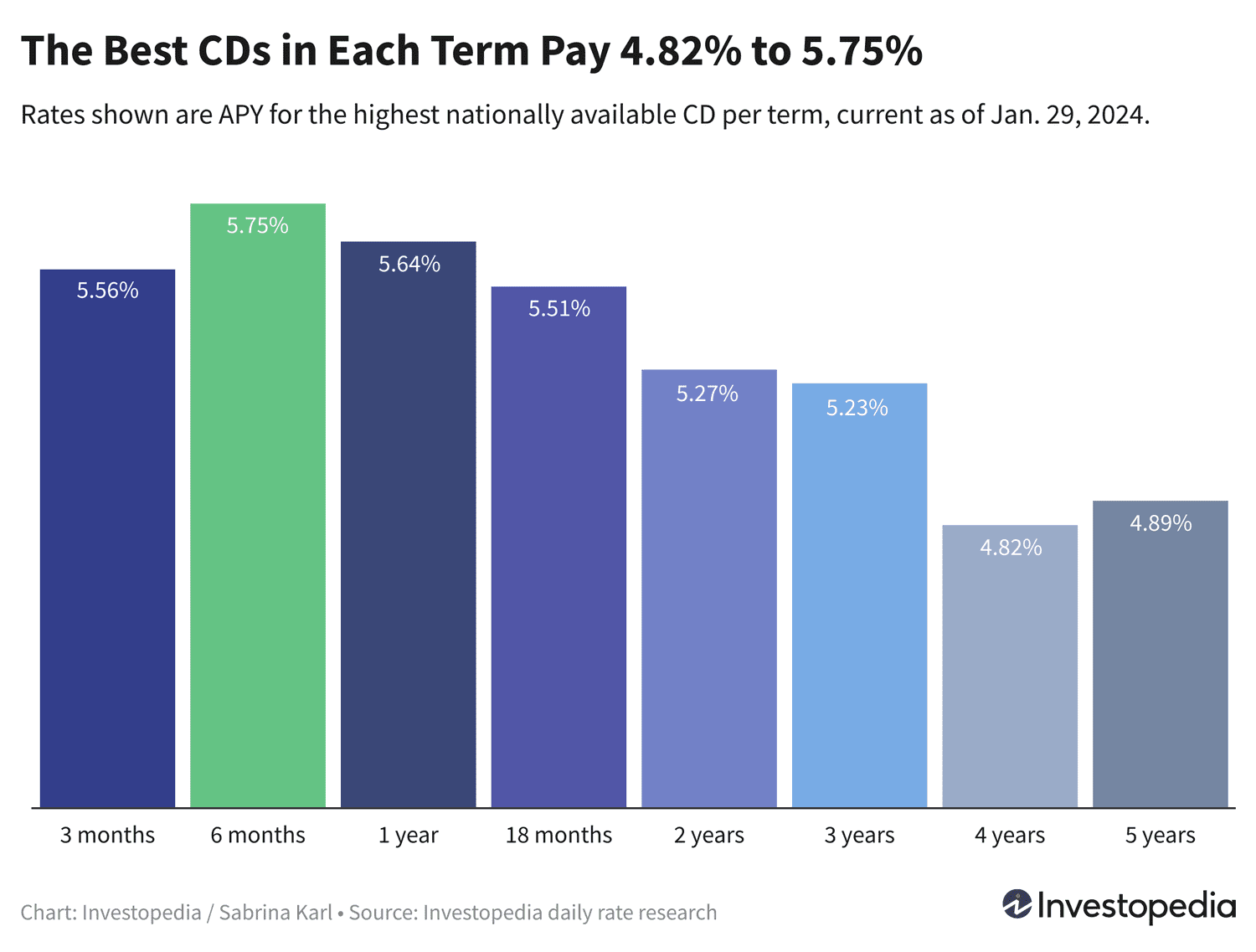

The best nationwide CD rate has increased to 5.75% for a 6-month offer from Andrews Federal Credit Union, with NASA Federal Credit Union offering 5.70% for 9 months. While rates have slightly decreased since October's peak, they remain historically high, with 34 CDs paying 5.50% or higher. The Fed is expected to lower interest rates, making it a good time to secure a high-paying CD. Longer-term CDs are also attractive, with a 2-year rate of 5.27% and 4-5 year offers in the upper 4% range. Jumbo CD rates vary, and it's important to compare standard and jumbo rates before deciding. The Fed's decisions on rates have significant implications for CD rates, and while predictions are uncertain, current rates are likely to plateau or decrease from their record highs.

In the current high-rate environment, short-term CDs are offering competitive rates, with 9-month CDs being particularly attractive. Several financial institutions are offering 9-month CD rates of up to 6.09% APY, with varying minimum deposit requirements and early withdrawal penalties. These short-term CDs can help savers achieve their financial goals and maximize interest returns, but it's important to ensure that the chosen account aligns with individual needs and requirements.

Certificate of deposit (CD) interest rates are currently at their highest in years, with the best one-year CDs offering 5.66% annual interest and the best six-month CDs topping out at 5.75%. While short-term CDs currently offer higher returns due to market forecasts of easing interest rates, investors should also consider longer terms as banks set CD rates based on their predictions of future interest rates. Opening a CD is relatively simple and can be done online, but investors must be willing to lock in their funds for the full term of the investment, and penalties apply for early withdrawals.