In 2025, US stocks performed well, but international markets outshined them, driven by AI growth in Asia, European economic reforms, and a weaker dollar, prompting investors to diversify globally amid ongoing US resilience.

Stocks experienced a pullback after a recent rally driven by AI optimism, with tech shares leading declines amid valuation concerns, prompting a shift to safer assets like bonds and currencies; global markets showed signs of overheating and vulnerability.

Global equities paused their rally amid concerns over overvalued tech stocks and a strong US dollar, with Asian markets declining and investors cautious ahead of key economic reports and political developments worldwide.

Global equities hit new highs as optimism grew over potential trade agreements between the US, Japan, and the EU, easing fears of a prolonged trade war and boosting investor confidence, with markets reacting positively to signs of de-escalation in trade tensions.

Global equities have outperformed U.S. stocks in 2025, driven by factors like currency movements, geopolitical shifts, and divergent fiscal policies, suggesting that international investments may continue to outperform U.S. assets despite recent market gains and trade tensions.

Global equity indices dipped slightly while U.S. Treasury yields rose as investors awaited key inflation data expected later in the week, which could provide insights into the Federal Reserve's interest rate outlook. U.S. consumer confidence improved unexpectedly, and house price growth slowed, adding to market uncertainty. The Nasdaq hit a record high, driven by Nvidia's performance, while the Dow and S&P 500 showed mixed results. Treasury yields increased following weak debt auctions, and the dollar strengthened slightly. Oil and gold prices also saw gains.

Global equities dipped slightly while U.S. Treasury yields rose to multi-week highs as investors awaited key inflation data expected to provide insights into U.S. interest rates. U.S. consumer confidence improved unexpectedly, and house price growth slowed. The Nasdaq hit a record high, driven by Nvidia's performance, while the Dow and S&P 500 showed mixed results. Treasury yields rose following weak debt auctions, and the dollar strengthened. Oil prices increased on expectations of OPEC+ maintaining supply curbs, and gold prices saw a slight rise.

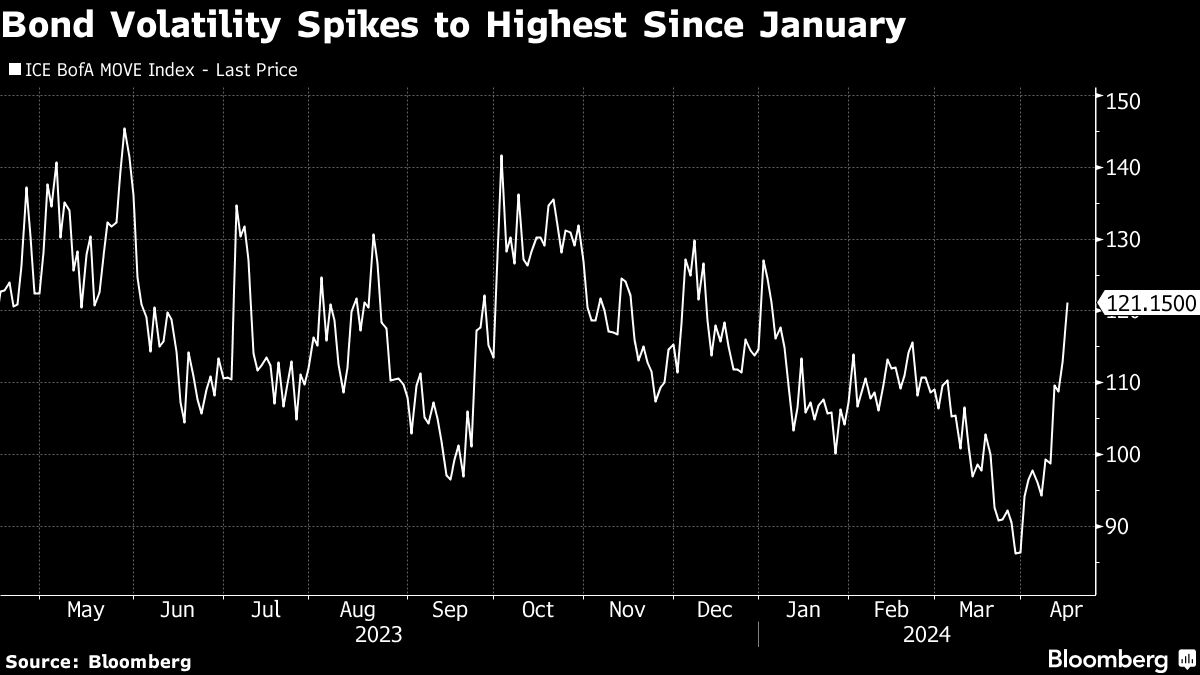

Global equities stabilized following a recent selloff, with Asian currencies in focus as traders prepared for the Federal Reserve's higher-for-longer interest rates. The dollar halted its ascent after a five-day gain, exerting pressure on global emerging-market currencies. Stock markets in Asia diverged, with losses in Japan offset by gains in mainland China. Treasury yields traded in a narrow range after climbing to fresh 2024 highs, and market-implied expectations for Fed rate cuts declined after Fed chief Jerome Powell's comments on inflation. Elsewhere, New Zealand home-grown price pressures persisted, and Asian liquefied natural gas prices jumped to the highest level since early January while oil edged lower.

Global equities are set for a second quarterly gain, with the S&P 500 closing at a record high, while Treasuries slipped after a Federal Reserve official indicated no rush to cut interest rates. MSCI Inc.'s global stocks index is on track to rise over 7% this quarter, buoyed by US and Japan rallies and the artificial intelligence sector, with Hon Hai Precision Industry Co. seeing a surge in Taiwan despite concerns over smartphone sector recovery.

Asian stocks rose for a second day, following a global rally in equities that saw markets in the US, Europe, and Japan hit all-time highs. Most notably, Nvidia's market capitalization surged, driven by the AI computing boom. The bullish mood in Asia was also supported by a buoyant outlook for Nvidia and strong economic data from the US. Meanwhile, China's economic slowdown and concerns about property-sector improvement were also in focus. In the US, traders took more hawkish Fed commentary in stride, and in commodities, oil slipped while gold fluctuated.

Stock futures in Europe and the US are on the rise, following the S&P 500's record-high close on Friday, driven by optimism over expected Federal Reserve interest-rate cuts and the artificial-intelligence boom. Chinese stocks, however, experienced losses due to concerns about the nation's faltering recovery. Additionally, oil prices fell as Libya restarted output at its largest field, and the dollar weakened against most of its peers. This week, investors will focus on the Bank of Japan's policy meeting, US fourth-quarter GDP estimate, and central bank meetings for Canada and Europe, among other key events.

Global equities remained steady as investors awaited key U.S. and European inflation data, while gold reached a six-month high due to a weakening dollar. European stocks were slightly lower, with the STOXX 600 index down 0.13%. The oil market faced uncertainty ahead of the delayed OPEC+ meeting, causing oil prices to slip. The market's focus is on the upcoming release of inflation figures and the Fed's preferred measure of inflation, which could provide direction for markets.

Most Asia-Pacific markets dipped in choppy trading, extending declines from the previous session. Japan's business sentiment improved for the first time since August, according to the Reuters Tankan survey. South Korean stocks retreated, while U.S. markets closed with their longest winning streaks in nearly two years. New Zealand's inflation expectations fell to a two-year low in the fourth quarter. Morgan Stanley highlighted the stocks that will benefit and lose out from the wellness trend. HSBC predicts a 15% rally in global equities if central banks ease monetary policy and the Federal Reserve manages a soft landing. Chicago Federal Reserve President Austan Goolsbee said a soft landing is still possible. U.S. crude prices fell to their lowest level since July due to weak economic data. Wolfe Research warns that the market rally may be fleeting.

CNBC's 13th annual Delivering Alpha investor summit brings together elite investors and money managers to discuss market moves and share top ideas on maximizing returns and navigating risks. A CNBC survey shows that a majority of Wall Street investors believe the stock market's gain this year has been a bear market bounce, with more trouble ahead. Goldman Sachs Asset Management CIO of public investing, Ashish Shah, suggests that investors can find better returns in international markets like India and Japan. Private equity valuations are expected to decline as more companies face cash crunches, according to Ariel Alternatives CEO Les Brun. Bill Ackman's comments at the summit could impact market sentiment.

Asian and European equity futures fell, while Treasury yields and the dollar rose, indicating that investors are still adjusting their interest rate expectations. US equity futures also declined, erasing Monday's gains on Wall Street. Chinese property concerns weighed on markets, with Hong Kong's Hang Seng Index falling to November levels. The MSCI All Country World Index is on track for its longest losing streak in a decade. Treasury yields continued to climb, reaching a 16-year high, and the dollar held its gains. Crude prices fell for a second session, and there are concerns that rising oil prices could fuel inflation. Federal Reserve officials have indicated the possibility of further interest rate increases this year.