Asia-Pacific markets rose ahead of China's key lending rate decisions, with major indices in Japan, South Korea, and Hong Kong gaining, while US stocks also increased driven by AI-related gains and corporate news.

Citigroup Inc. strategists have downgraded their outlook on the US tech sector, shifting to a more cautious stance and reducing their recommendation to market-weight from overweight, while also issuing an underweight recommendation on hardware companies. They anticipate the stock rally to broaden beyond technology and have raised their outlook on consumer discretionary to overweight.

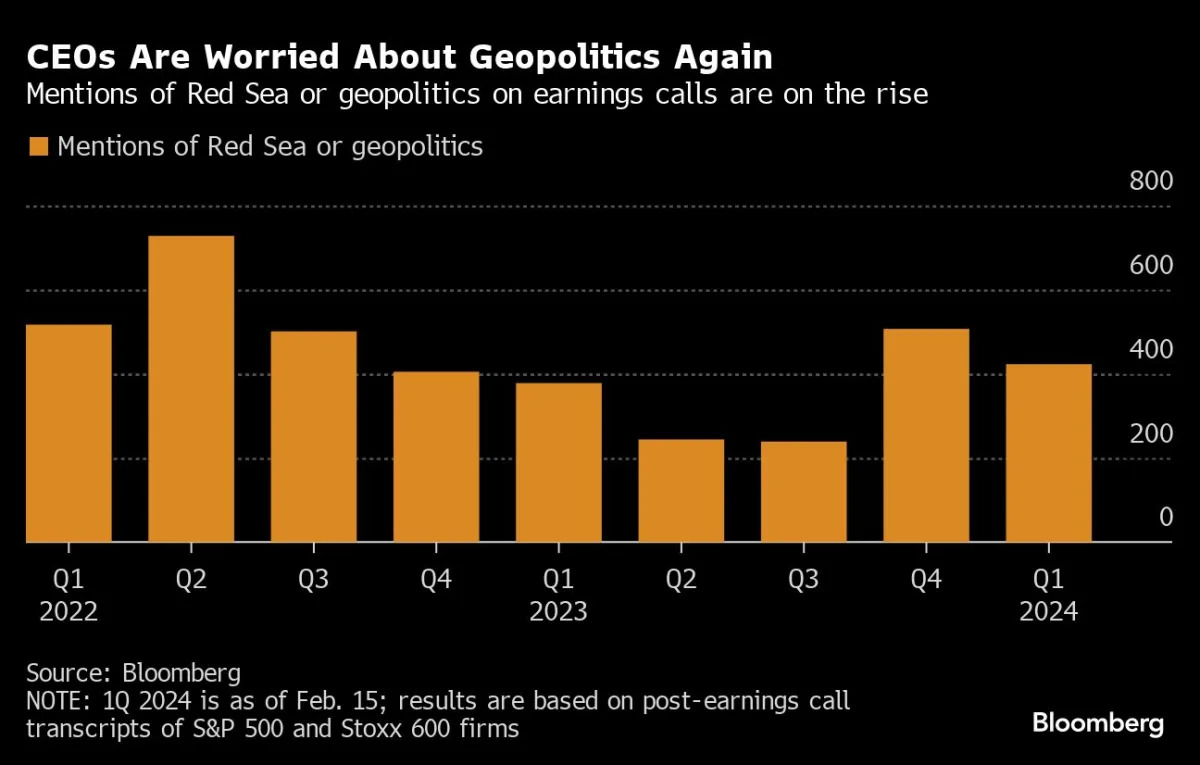

The record rally in US stocks is facing threats from the ongoing conflict in the Middle East, with companies and investors expressing concerns about the impact on earnings due to boycotts, supply chain disruptions, and rising geopolitical tensions. References to the Red Sea and geopolitics in earnings calls have surged, and expectations for S&P 500 profits are at a record high. The war's potential to affect corporate margins, inflation, and supply costs has led to worries about the sustainability of the stock rally, with some firms already experiencing negative impacts while others have seen increased demand. Shoppers in the Middle East and Muslim nations are boycotting major US brands, further impacting earnings, and the conflict shows no signs of abating.