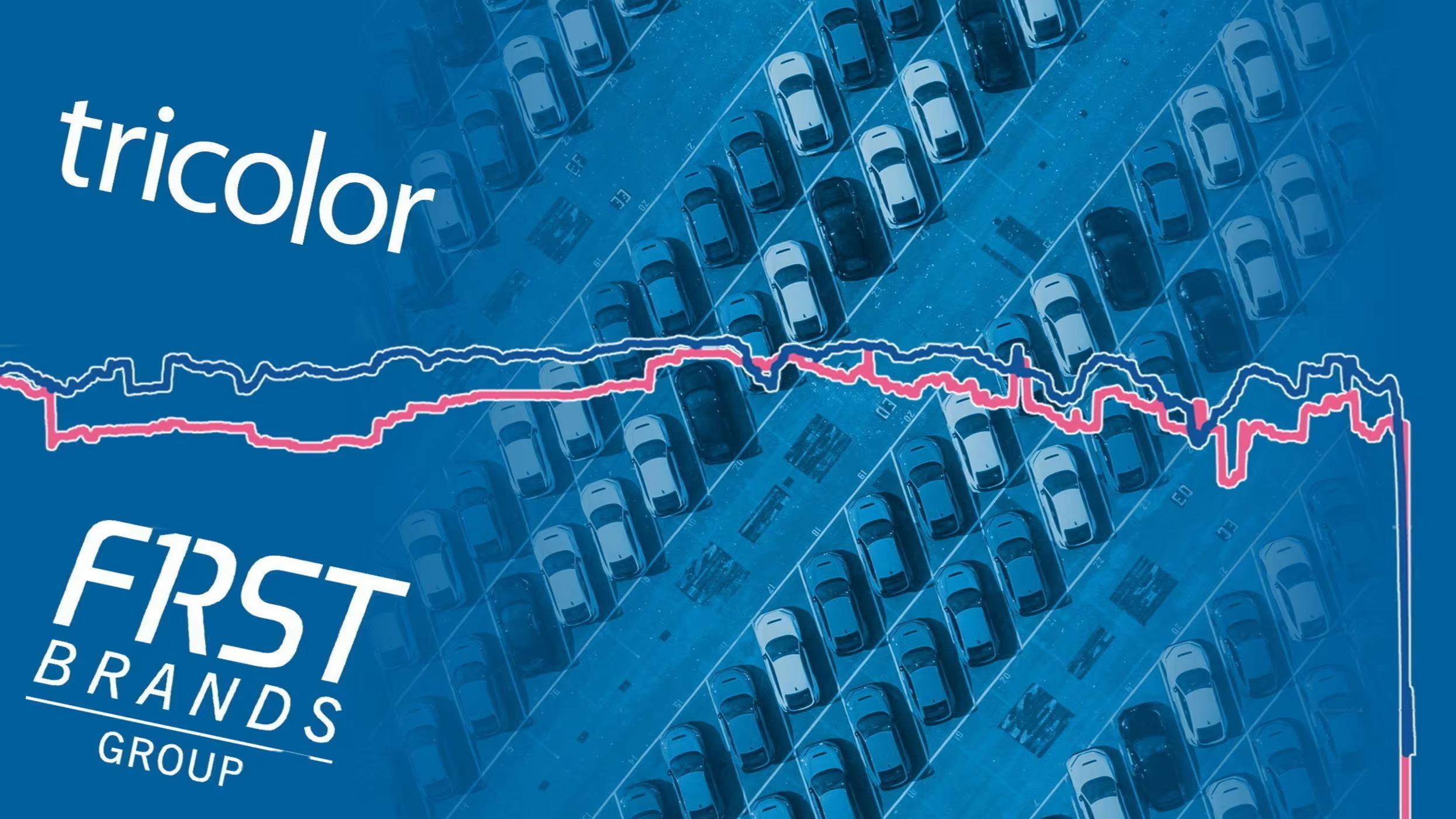

Investors are warning about the risks associated with leveraged loans following the collapse of First Brands, highlighting concerns over financial stability and potential widespread impacts.

Companies sold a record volume of leveraged loans last month, but recovery rates for defaults have significantly dropped. Investors in newly issued first-lien debt in the US and Canada can now expect to recover less than 35% of their investment, compared to 72% from 2018-2022, highlighting increased risk in this debt market.

Companies in the U.S. leveraged loan market could face distress if the Federal Reserve maintains high interest rates, according to Oaktree Capital Management. Elevated interest rates are making it challenging for companies to service their floating-rate debt, potentially leading to defaults. Moody's Investors Service estimates that about 62% of B-rated companies would struggle to pay interest on their debts if the Fed's policy rate remains unchanged. While leveraged loan defaults have been rising, total returns have remained positive. However, if the Fed keeps rates high for longer, the grace period for borrowers will narrow, exposing a significant portion of the sector to higher borrowing costs. Investors should prepare for potential disruptions in credit markets and consider buying opportunities.

Leveraged loan defaults have reached $24.5 billion, putting the sector on track for the third-worst year in history, according to Goldman Sachs. The rise in defaults is due to the Federal Reserve's interest rate hikes, which have hit borrowers with floating-rate debt particularly hard. Leveraged loans are high-risk financing for companies with substantial debt and poor credit histories, and have given rise to leveraged corporate buyouts. The sector has also produced collateralized loan obligations and exchange-traded funds.