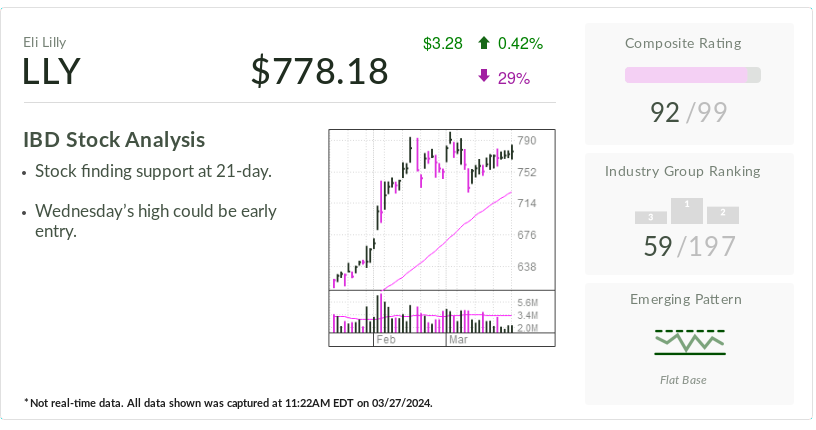

HSBC Downgrades Lilly as Obesity Market Faces Pricing Pressures

HSBC analyst Rajesh Kumar downgraded Eli Lilly (LLY) from Hold to Sell, arguing that pricing dynamics and a downsized total addressable market, intensified competition from Novo Nordisk, and potential headwinds for Lilly’s oral obesity drug orforglipron could limit upside; he cut the price target from $1,070 to $850 as TAM is viewed at about $80–120B versus consensus around $150B+, while the broader market remains bullish with a Strong Buy consensus and ~36% upside over the next year.